analysis of market price gdp per capita across european countries

comparing GDP per capita across European countries in 2014, and pulling in a few country-level factors to see what lines up with it.

| Dataset | Year | Description | Source |

|---|---|---|---|

| nama_10_pc | 2014 | Main GDP aggregates per capita (eurostat database) | [src] |

# .libPaths('/tmp')

# install.packages("eurostat")

# install.packages("ggplot2")

# install.packages("GGally")

# install.packages("car")

# install.packages("lmtest")

library(eurostat)

library(ggplot2)

library(GGally)

library(car)

library(MASS)

library(lmtest)

id <- "nama_10_pc"

df <- get_eurostat(id = id)

hdp <- subset(df, TIME_PERIOD == "2014-01-01")

hdp <- subset(hdp, na_item == "B1GQ")

hdp <- subset(hdp, unit == "CP_EUR_HAB")

hdp <- subset(hdp, select = c("geo", "values"))

hdp <- subset(hdp, !grepl("^EA", geo))

hdp <- subset(hdp, !grepl("^EU", geo))

hdp <- label_eurostat(hdp)

Table nama_10_pc cached at /tmp/Rtmp5jJlAc/eurostat/75bde536dea5c4c637c89baee219dd46.rds

Main GDP aggregates per capita

- Code:

nama_10_pc - Time: 2014

- Time frequency: Annual

- National accounts indicator: Gross domestic product at market prices

- Unit of measure: Current prices, euro per capita

hdp$geo

- 'Albania'

- 'Austria'

- 'Belgium'

- 'Bulgaria'

- 'Switzerland'

- 'Cyprus'

- 'Czechia'

- 'Germany'

- 'Denmark'

- 'Estonia'

- 'Greece'

- 'Spain'

- 'Finland'

- 'France'

- 'Croatia'

- 'Hungary'

- 'Ireland'

- 'Iceland'

- 'Italy'

- 'Liechtenstein'

- 'Lithuania'

- 'Luxembourg'

- 'Latvia'

- 'Montenegro'

- 'North Macedonia'

- 'Malta'

- 'Netherlands'

- 'Norway'

- 'Poland'

- 'Portugal'

- 'Romania'

- 'Serbia'

- 'Sweden'

- 'Slovenia'

- 'Slovakia'

- 'Türkiye'

- 'United Kingdom'

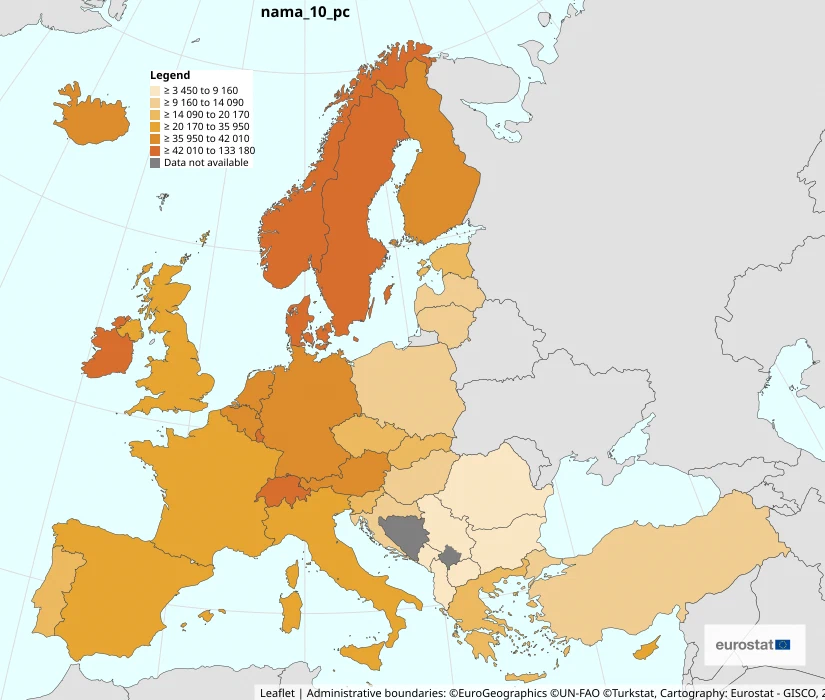

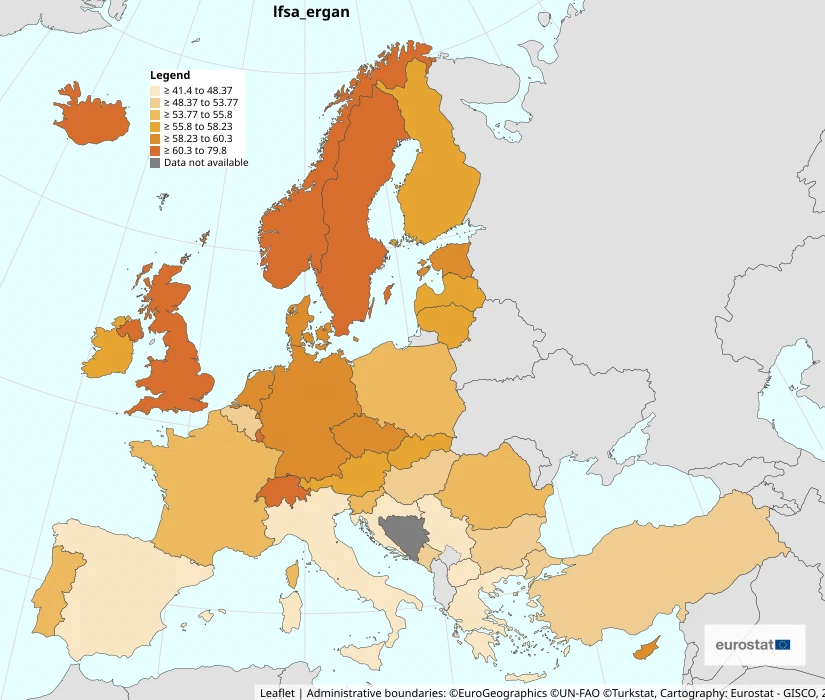

the Nordic countries, plus Ireland, Switzerland, and Luxembourg, top the GDP per capita list. Western Europe sits high too. the lowest values are in Eastern Europe.

data description

we look at the GDP of European countries in 2014, in euros per capita (CP_EUR_HAB) at market prices (B1GQ).

options(repr.plot.width = 10, repr.plot.height = 6)

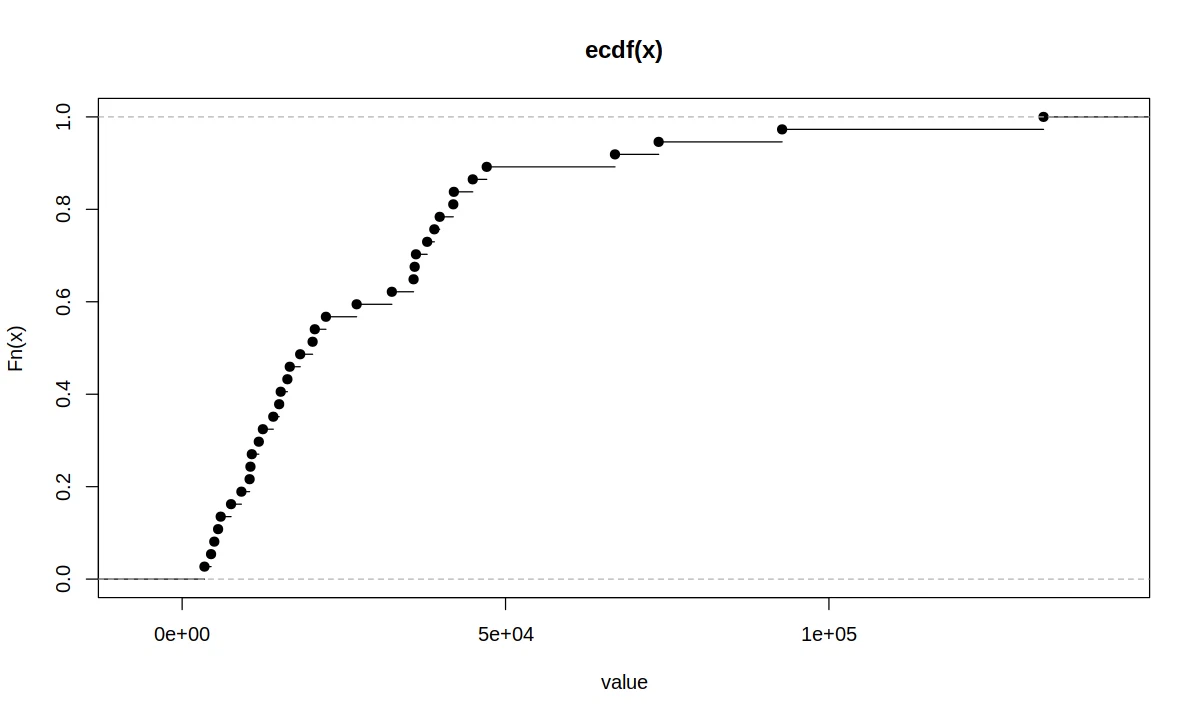

plot.ecdf(hdp$values, xlab = "value")

options(repr.plot.width = 10, repr.plot.height = 6)

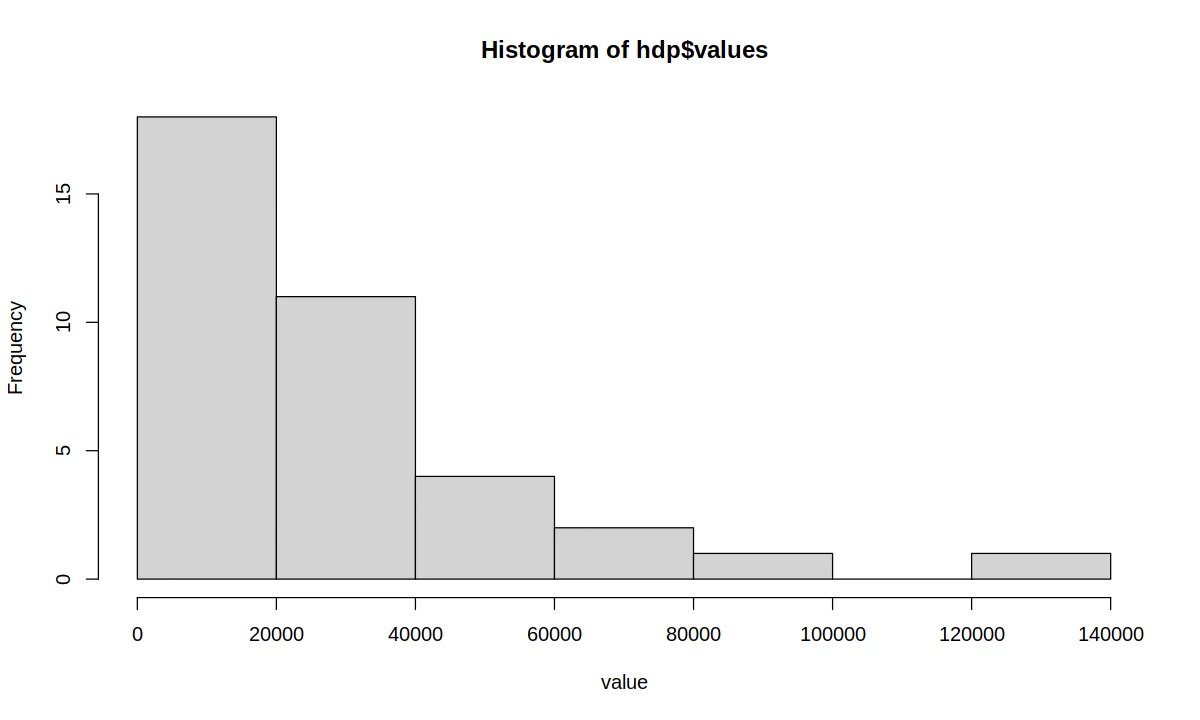

hist(hdp$values, breaks = 9, xlab = "value")

head(hdp[order(hdp$values, decreasing = T), ], 5)

tail(hdp[order(hdp$values, decreasing = T), ], 5)

options(repr.plot.width = 10, repr.plot.height = 3)

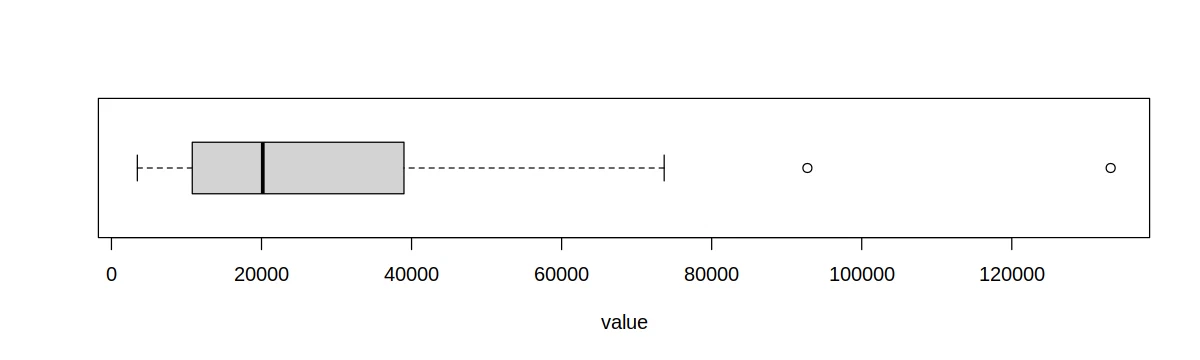

boxplot(hdp$values, horizontal = T, xlab = "value")

| geo | values |

|---|---|

| <chr> | <dbl> |

| Liechtenstein | 133180 |

| Luxembourg | 92760 |

| Norway | 73670 |

| Switzerland | 66920 |

| Denmark | 47090 |

| geo | values |

|---|---|

| <chr> | <dbl> |

| Bulgaria | 5960 |

| Montenegro | 5560 |

| Serbia | 4970 |

| North Macedonia | 4470 |

| Albania | 3450 |

cat("Count:", length(hdp$values), "\n")

cat("Var:", var(hdp$values), "\n")

cat("Std:", sd(hdp$values), "\n")

summary(hdp$values)

Count: 37

Var: 730769837

Std: 27032.75

Min. 1st Qu. Median Mean 3rd Qu. Max.

3450 10770 20170 29245 38990 133180

we see that only a few countries have very high GDP per capita, most sit in the 1,000 to 4,000 EUR range.

factors affecting GDP

GDP is shaped by a lot of things, here are some. the bolded ones are the regressors used in the next section.

economy and trade

- Inflation and interest rates influence consumer and investor confidence. low inflation boosts confidence and helps growth.

- Exports and imports. high exports point to a strong, self-sufficient economy. high imports hint at dependence on foreign trade and possible imbalance.

labor market

- Employment. higher employment usually means higher GDP, more people with income and purchasing power.

- Income levels. job quality matters too, not just having one. lots of low-wage jobs doesn’t necessarily lift GDP per capita. people earning more tend to spend more on goods and services.

other factors

Happiness and satisfaction. a happier population usually performs better at work and tends to help growth.

Adaptation to technological changes. a country’s ability to absorb new tech boosts competitiveness and productivity, and opens up new opportunities in production, services, and trade.

Climatic conditions. floods, droughts, or extreme temperatures can hurt agriculture and infrastructure. favorable climates support industries like tourism and agriculture.

indicators

the regressors we use are

- Employment rate

- Average monthly income

- Internet usage

- Climate region

next we look at the key properties of these indicators and how they relate to GDP.

all indicators are statistically significant and explain the modeled variable well. at the standard significance level we reject the hypothesis that the correlation between each regressor and GDP is zero.

id <- "lfsa_ergan"

emp <- get_eurostat(id = id)

emp <- subset(emp, TIME_PERIOD == "2014-01-01")

emp <- subset(emp, sex == "T")

emp <- subset(emp, citizen == "TOTAL")

emp <- subset(emp, age == "Y_GE25")

emp <- subset(emp, !grepl("^EU", geo))

emp <- subset(emp, !grepl("^EA", geo))

emp <- subset(emp, select = c("geo", "values"))

emp <- label_eurostat(emp)

# https://data.worldbank.org/indicator/SL.EMP.TOTL.SP.NE.ZS?locations=LI-AL

emp <- rbind(emp, c("Albania", 43.8))

emp <- rbind(emp, c("Liechtenstein", 59.4))

# ===========================================

id <- "earn_ses14_19"

earn <- get_eurostat(id = id)

earn <- subset(earn, cpayagr == "TOTAL")

earn <- subset(earn, currency == "EUR")

earn <- subset(earn, sizeclas == "GE10")

earn <- subset(earn, TIME_PERIOD == "2014-01-01")

earn <- subset(earn, indic_se == "ERN")

earn <- subset(earn, sex == "T")

earn <- subset(earn, nace_r2 == "B-S_X_O")

earn <- subset(earn, !grepl("^EU", geo))

earn <- subset(earn, !grepl("^EA", geo))

earn <- subset(earn, select = c("geo", "values"))

earn <- label_eurostat(earn)

# https://ndiqparate.al/?p=9775&lang=en

earn <- rbind(earn, c("Albania", 480))

# https://archiv.llv.li/files/as/jahrbuch-2017.pdf (p. 121)

earn <- rbind(earn, c("Liechtenstein", 6692))

# ===========================================

id <- "tin00028"

int <- get_eurostat(id = id)

int <- subset(int, indic_is == "I_IU3")

int <- subset(int, TIME_PERIOD == "2014-01-01")

int <- subset(int, !grepl("^EU", geo))

int <- subset(int, !grepl("^EA", geo))

int <- subset(int, select = c("geo", "values"))

int <- label_eurostat(int)

# https://data.worldbank.org/indicator/IT.NET.USER.ZS?locations=AL-LI-ME-RS

int <- rbind(int, c("Albania", 54))

int <- rbind(int, c("Liechtenstein", 95))

int <- rbind(int, c("Montenegro", 61))

int <- rbind(int, c("Serbia", 62))

# ===========================================

countries <- c(

"Albania", "Greece", "Italy", "Cyprus", "Croatia", "Spain", "North Macedonia", "Malta",

"Slovenia", "Serbia", "Türkiye", "Montenegro", "Portugal",

"Austria", "Belgium", "Bulgaria", "Switzerland", "Liechtenstein", "Luxembourg", "Netherlands",

"Slovakia", "United Kingdom", "Poland", "Romania", "Czechia", "Germany", "France", "Hungary",

"Ireland",

"Denmark", "Estonia", "Finland", "Iceland", "Latvia", "Lithuania", "Norway", "Sweden"

)

climate_zones <- c(rep("Mediterranean climate", 13), rep("Temperate", 16), rep("Cold", 8))

clima <- data.frame(geo = countries, climate = climate_zones)

# ===========================================

colnames(emp)[colnames(emp) == "values"] <- "employment"

colnames(earn)[colnames(earn) == "values"] <- "earnings"

colnames(int)[colnames(int) == "values"] <- "internet"

colnames(clima)[colnames(clima) == "values"] <- "climate"

df <- merge(hdp, emp, by = "geo")

df <- merge(df, earn, by = "geo")

df <- merge(df, int, by = "geo")

df <- merge(df, clima, by = "geo")

df$employment <- as.double(df$employment)

df$earnings <- as.double(df$earnings)

df$internet <- as.double(df$internet)

df$climate <- as.factor(df$climate)

Table lfsa_ergan cached at /tmp/Rtmp5jJlAc/eurostat/6f0b206586a43436eb71f5af3e1aa2e0.rds

Table earn_ses14_19 cached at /tmp/Rtmp5jJlAc/eurostat/499f0f870ce46c24042e585f1a785759.rds

Table tin00028 cached at /tmp/Rtmp5jJlAc/eurostat/8820f6902667cc62164e76efda7ba3ce.rds

employment rate

- Code:

lfsa_ergan - Name: Employment rates by sex, age and citizenship

- Time: 2014

- Sex: Total

- Age: 25 years and over

- Country of citizenship: Total

- Time frequency: Annual

- Unit of measure: Percentage

head(df[order(df$employment, decreasing = T), c("geo", "employment")], 5)

tail(df[order(df$employment, decreasing = T), c("geo", "employment")], 5)

| geo | employment | |

|---|---|---|

| <chr> | <dbl> | |

| 15 | Iceland | 79.8 |

| 35 | Switzerland | 65.0 |

| 26 | Norway | 64.9 |

| 34 | Sweden | 62.6 |

| 21 | Luxembourg | 62.3 |

| geo | employment | |

|---|---|---|

| <chr> | <dbl> | |

| 17 | Italy | 46.4 |

| 30 | Serbia | 46.1 |

| 25 | North Macedonia | 45.4 |

| 1 | Albania | 43.8 |

| 13 | Greece | 41.4 |

regressor analysis

cat("Var:", var(df$employment), "\n")

cat("Std:", sd(df$employment), "\n")

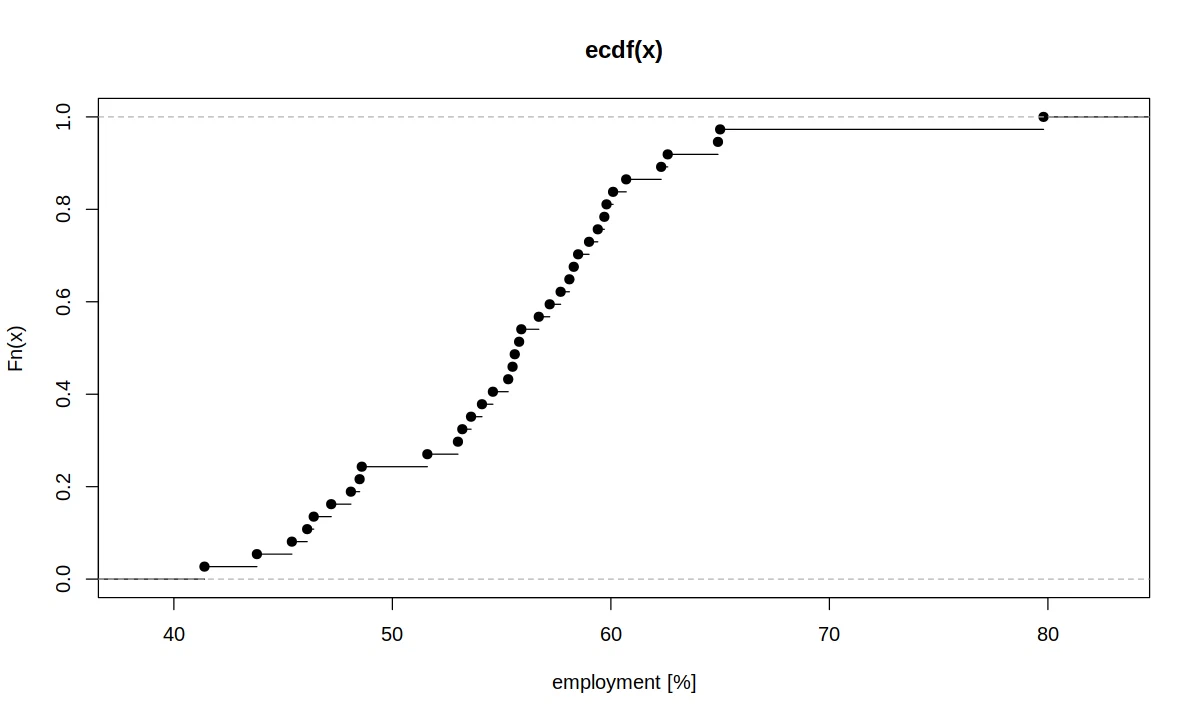

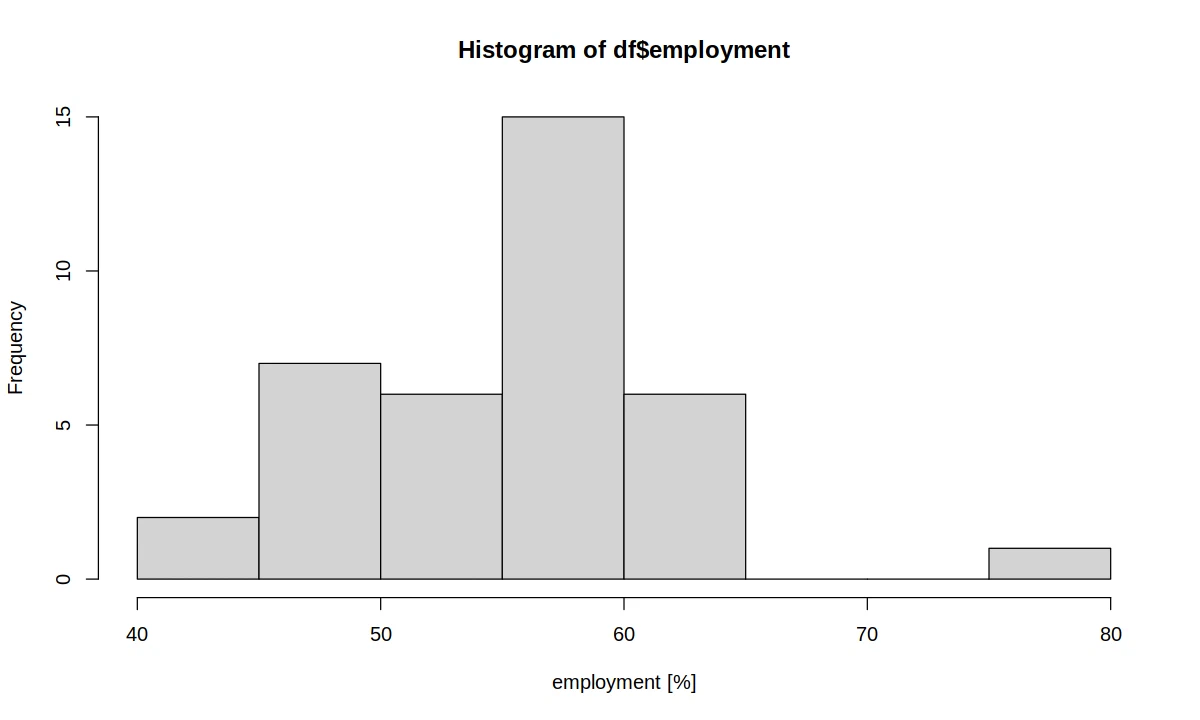

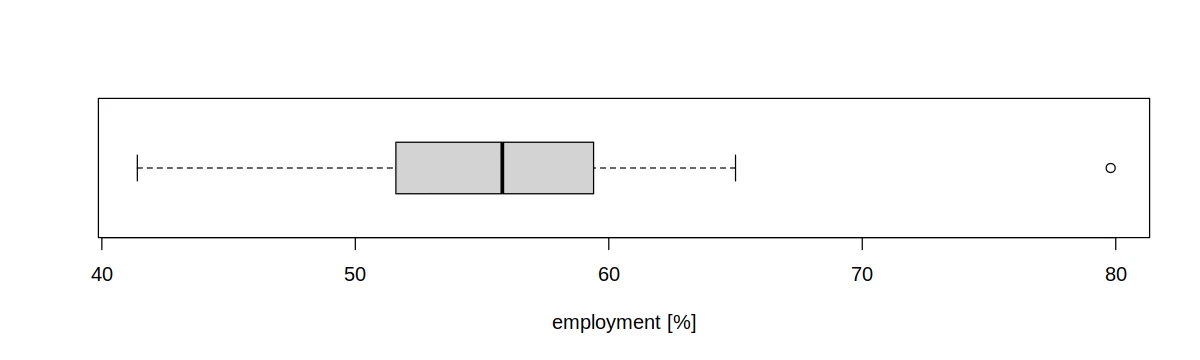

summary(df$employment)

Var: 52.02444

Std: 7.212797

Min. 1st Qu. Median Mean 3rd Qu. Max.

41.4 51.6 55.8 55.5 59.4 79.8

options(repr.plot.width = 10, repr.plot.height = 6)

plot.ecdf(df$employment, xlab = "employment [%]")

options(repr.plot.width = 10, repr.plot.height = 6)

hist(df$employment, xlab = "employment [%]")

options(repr.plot.width = 10, repr.plot.height = 3)

boxplot(df$employment, horizontal = T, xlab = "employment [%]")

dependence on GDP

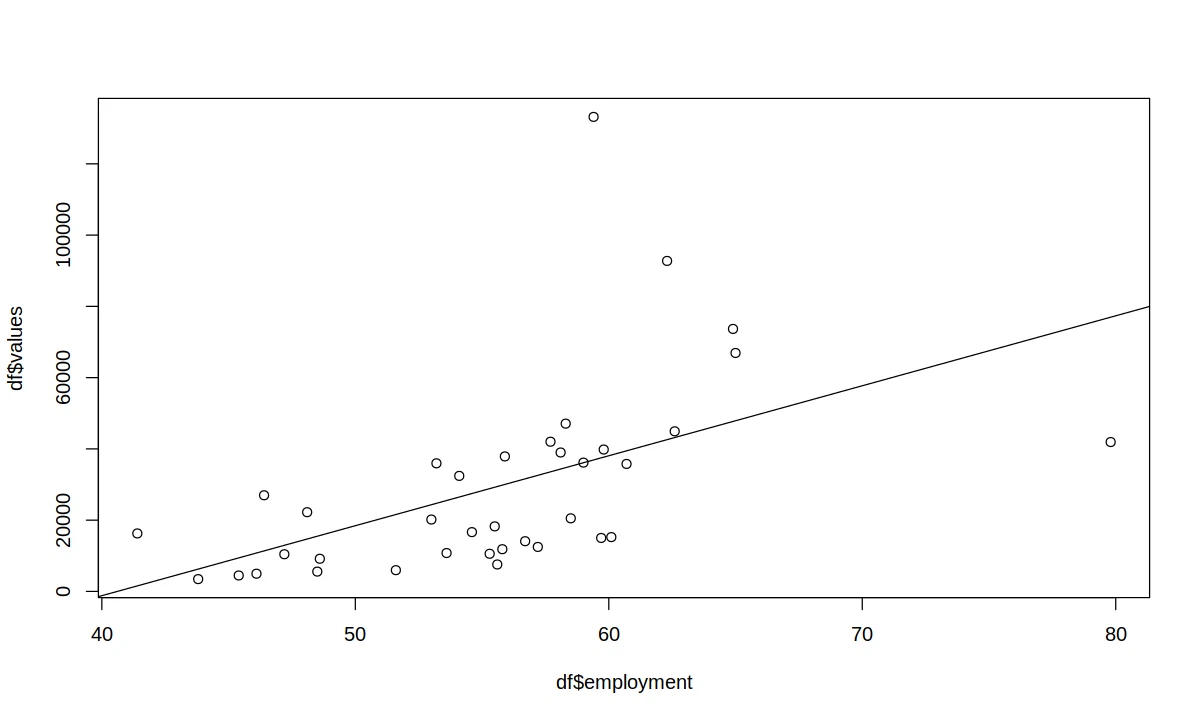

cor.test(df$values, df$employment)

Pearson's product-moment correlation

data: df$values and df$employment

t = 3.6397, df = 35, p-value = 0.0008728

alternative hypothesis: true correlation is not equal to 0

95 percent confidence interval:

0.2408721 0.7249318

sample estimates:

cor

0.5239948

fit <- lm(df$values ~ df$employment)

summary(fit)

options(repr.plot.width = 10, repr.plot.height = 6)

plot(df$values ~ df$employment)

abline(fit)

Call:

lm(formula = df$values ~ df$employment)

Residuals:

Min 1Q Median 3Q Max

-35047 -14744 -3677 7849 96276

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -79749.9 30191.4 -2.641 0.012255 *

df$employment 1963.9 539.6 3.640 0.000873 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 23350 on 35 degrees of freedom

Multiple R-squared: 0.2746, Adjusted R-squared: 0.2538

F-statistic: 13.25 on 1 and 35 DF, p-value: 0.0008728

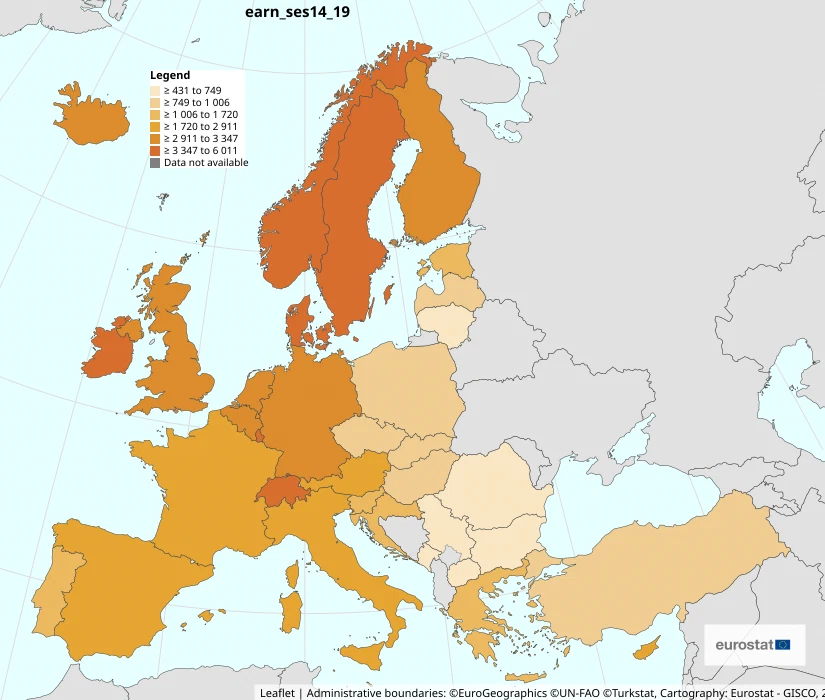

average monthly income

- Code:

earn_ses14_19 - Name: Mean monthly earnings by sex, economic activity and collective pay agreement

- Time: 2014

- Sex: Total

- collective pay agreement: Total

- Currency: Euro

- Economic activities: Industry, construction and services

- Indicator: Gross earnings

- Time frequency: Annual

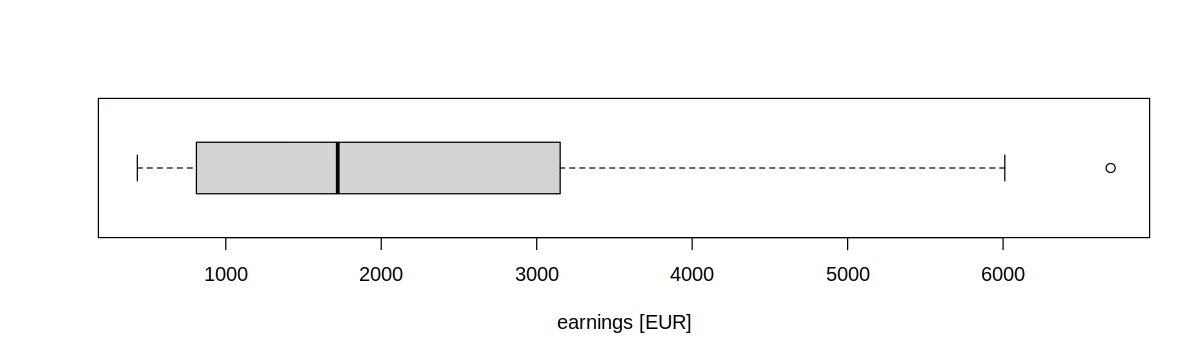

head(df[order(df$earnings, decreasing = T), c("geo", "earnings")], 5)

tail(df[order(df$earnings, decreasing = T), c("geo", "earnings")], 5)

| geo | earnings | |

|---|---|---|

| <chr> | <dbl> | |

| 19 | Liechtenstein | 6692 |

| 35 | Switzerland | 6011 |

| 26 | Norway | 5031 |

| 21 | Luxembourg | 4206 |

| 8 | Denmark | 4194 |

| geo | earnings | |

|---|---|---|

| <chr> | <dbl> | |

| 30 | Serbia | 574 |

| 29 | Romania | 521 |

| 25 | North Macedonia | 494 |

| 1 | Albania | 480 |

| 4 | Bulgaria | 431 |

regressor analysis

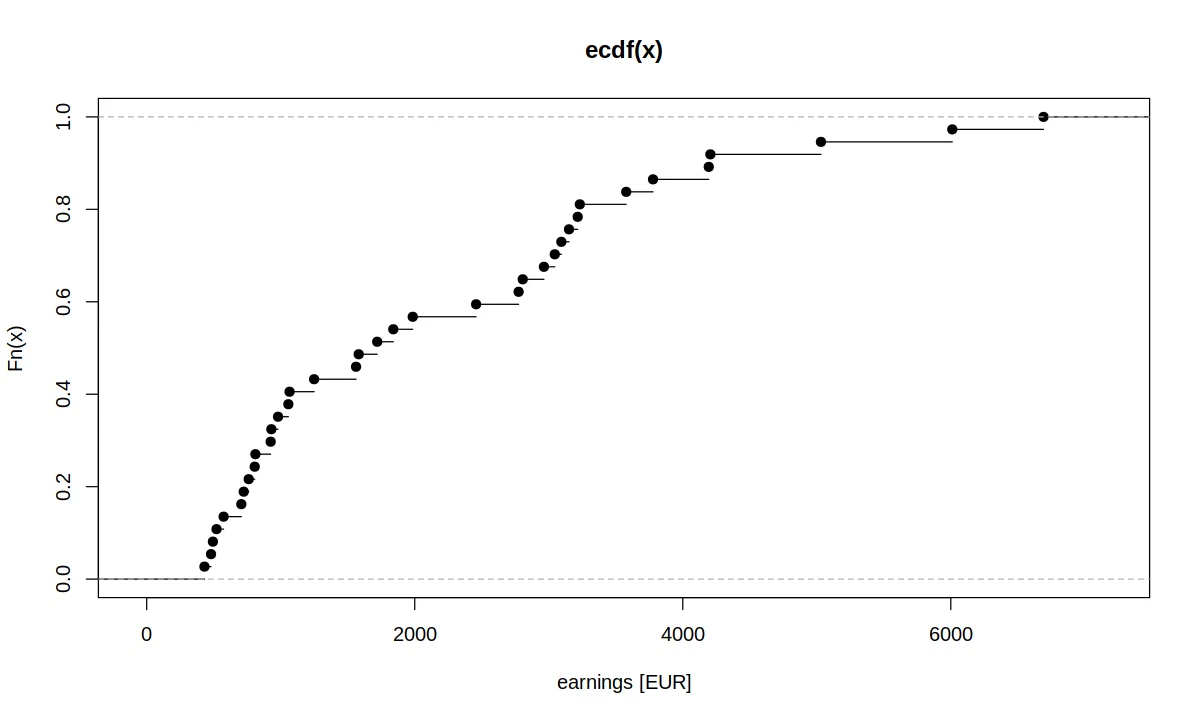

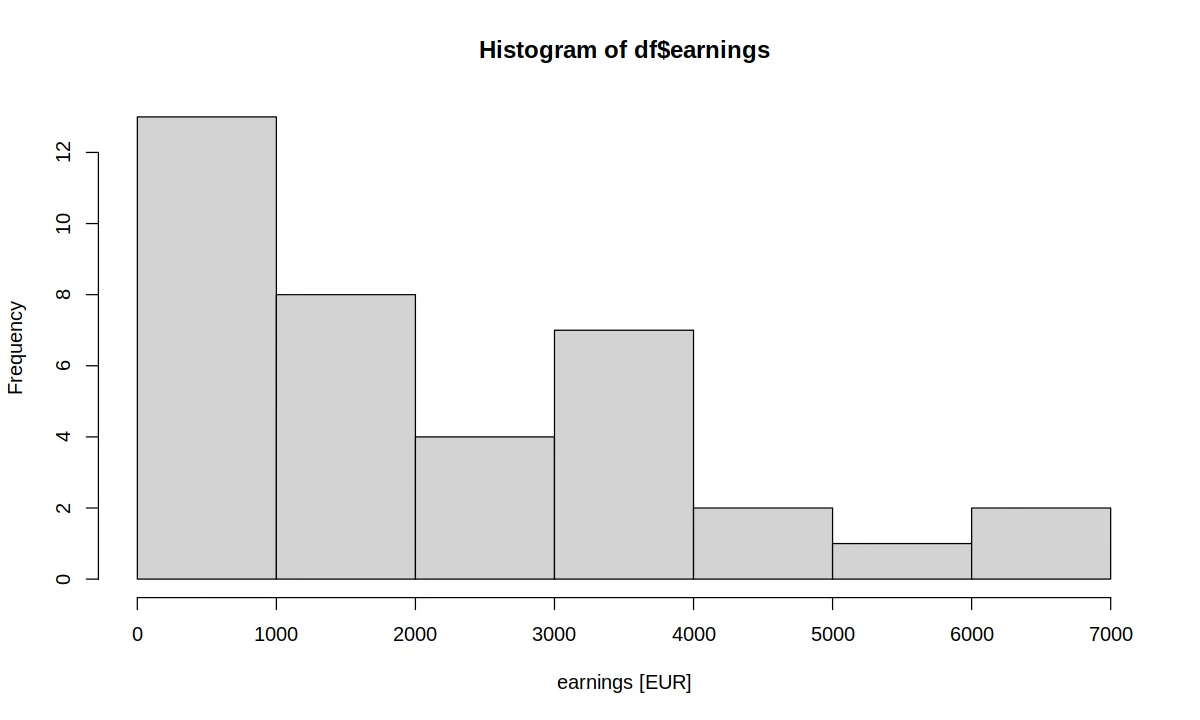

cat("Var:", var(df$earnings), "\n")

cat("Std:", sd(df$earnings), "\n")

summary(df$earnings)

Var: 2644510

Std: 1626.195

Min. 1st Qu. Median Mean 3rd Qu. Max.

431 811 1720 2201 3151 6692

options(repr.plot.width = 10, repr.plot.height = 6)

plot.ecdf(df$earnings, xlab = "earnings [EUR]")

options(repr.plot.width = 10, repr.plot.height = 6)

hist(df$earnings, xlab = "earnings [EUR]")

options(repr.plot.width = 10, repr.plot.height = 3)

boxplot(df$earnings, horizontal = T, xlab = "earnings [EUR]")

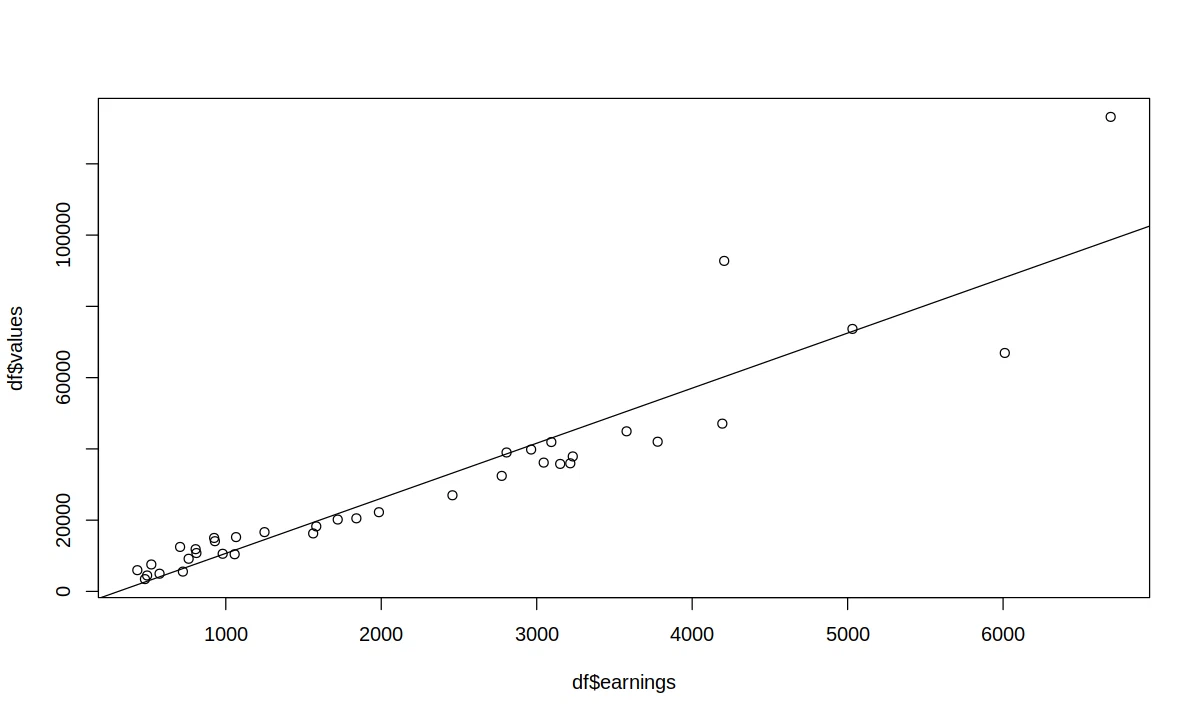

dependence on GDP

cor.test(df$values, df$earnings)

Pearson's product-moment correlation

data: df$values and df$earnings

t = 14.946, df = 35, p-value < 2.2e-16

alternative hypothesis: true correlation is not equal to 0

95 percent confidence interval:

0.8669865 0.9635352

sample estimates:

cor

0.9298047

fit <- lm(df$values ~ df$earnings)

summary(fit)

options(repr.plot.width = 10, repr.plot.height = 6)

plot(df$values ~ df$earnings)

abline(fit)

Call:

lm(formula = df$values ~ df$earnings)

Residuals:

Min 1Q Median 3Q Max

-21215 -5599 -857 3008 34519

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -4773.653 2816.531 -1.695 0.099 .

df$earnings 15.456 1.034 14.946 <2e-16 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 10090 on 35 degrees of freedom

Multiple R-squared: 0.8645, Adjusted R-squared: 0.8607

F-statistic: 223.4 on 1 and 35 DF, p-value: < 2.2e-16

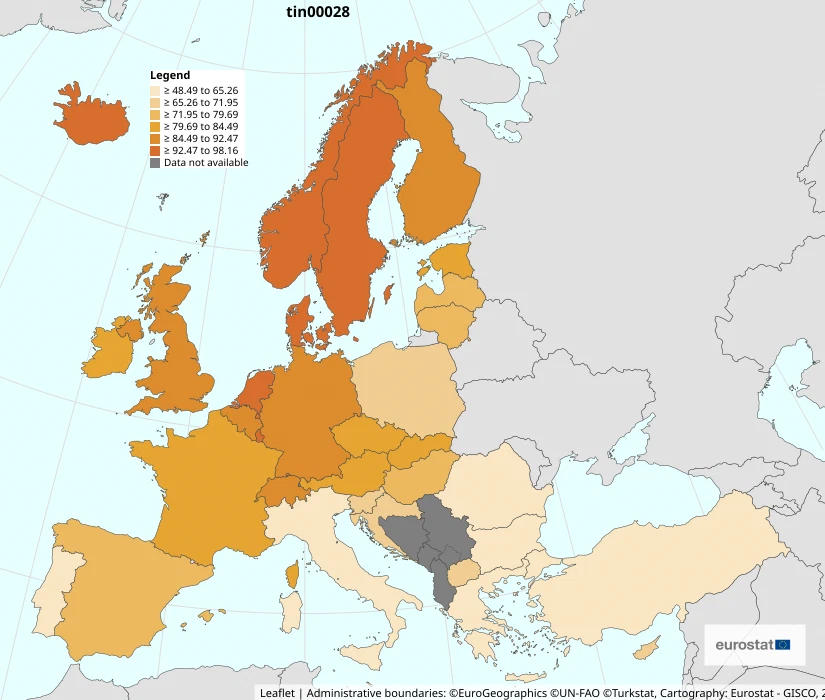

internet use by individuals

- Code:

tin00028 - Name: Internet use by individuals

- Time: 2014

- Individual type: All individuals

- Last internet use: in last 3 months

- Time frequency: Annual

- Unit of measure: Percantage of individuals

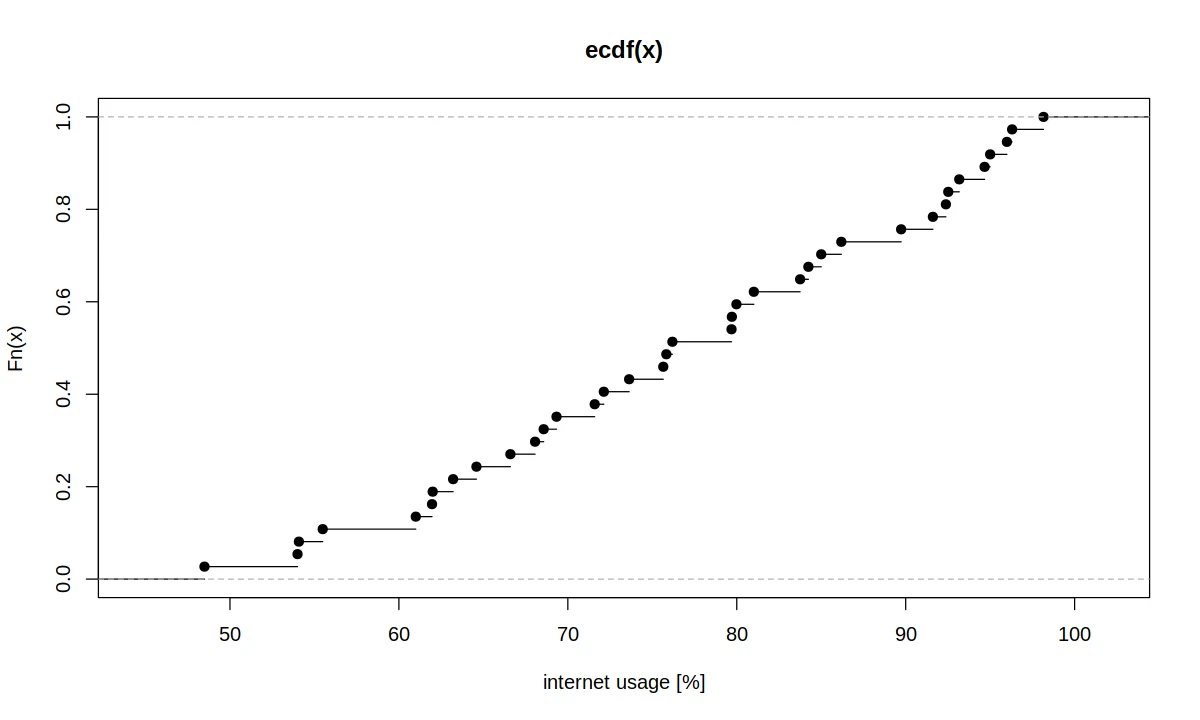

regressor analysis

cat("Var:", var(df$internet), "\n")

cat("Std:", sd(df$internet), "\n")

summary(df$internet)

Var: 193.9805

Std: 13.92769

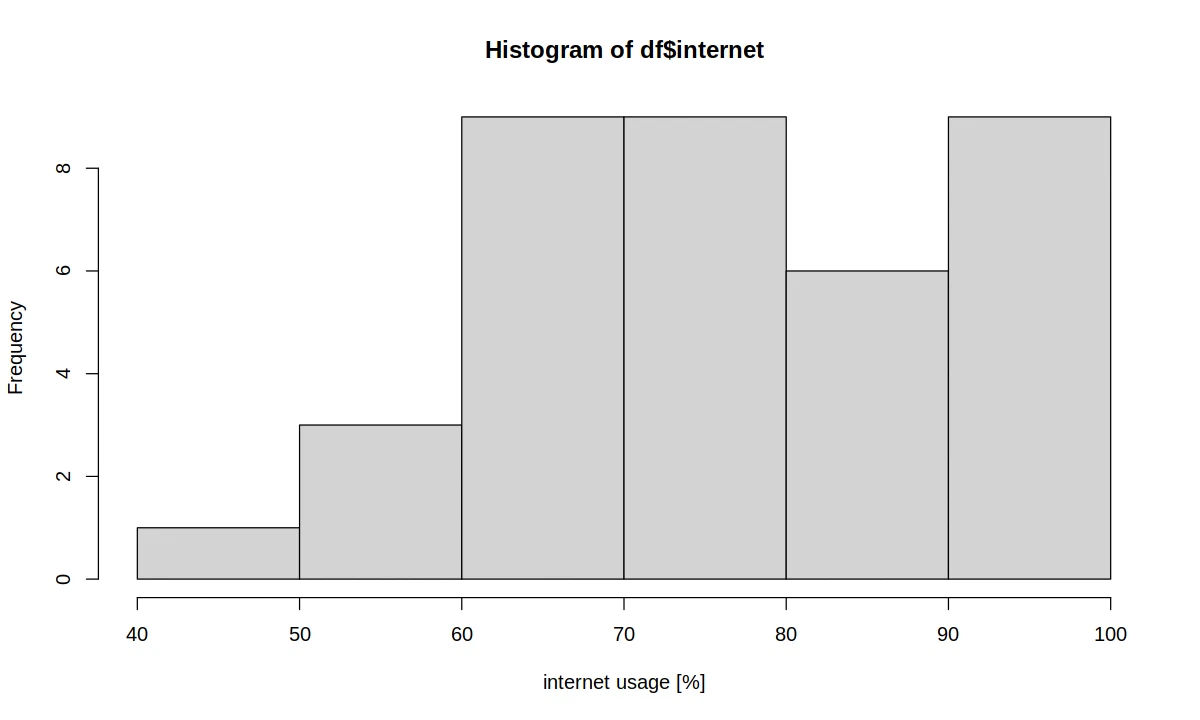

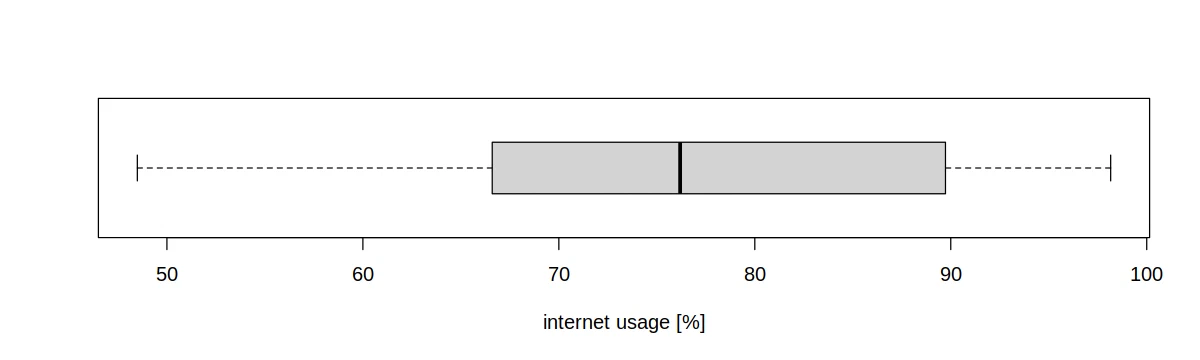

Min. 1st Qu. Median Mean 3rd Qu. Max.

48.49 66.60 76.19 76.80 89.73 98.16

options(repr.plot.width = 10, repr.plot.height = 6)

plot.ecdf(df$internet, xlab = "internet usage [%]")

options(repr.plot.width = 10, repr.plot.height = 6)

hist(df$internet, xlab = "internet usage [%]")

options(repr.plot.width = 10, repr.plot.height = 3)

boxplot(df$internet, horizontal = T, xlab = "internet usage [%]")

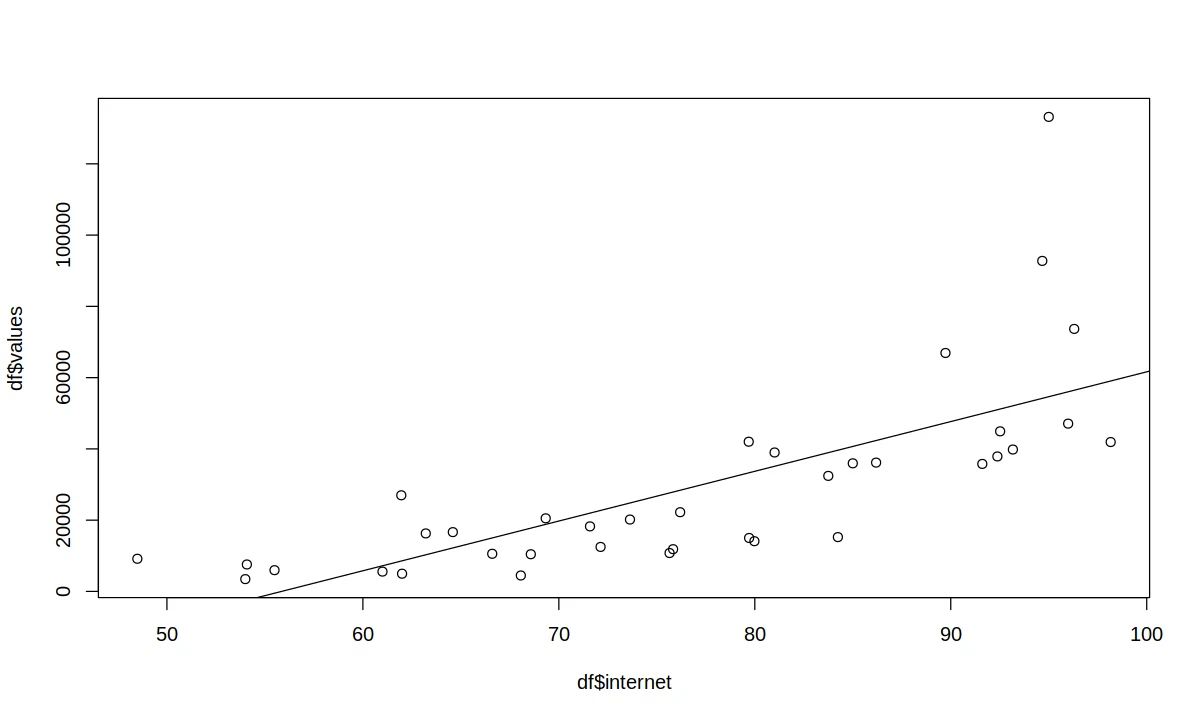

dependence on GDP

cor.test(df$values, df$internet)

Pearson's product-moment correlation

data: df$values and df$internet

t = 6.1225, df = 35, p-value = 5.327e-07

alternative hypothesis: true correlation is not equal to 0

95 percent confidence interval:

0.5151387 0.8460142

sample estimates:

cor

0.7191251

fit <- lm(df$values ~ df$internet)

summary(fit)

options(repr.plot.width = 10, repr.plot.height = 6)

plot(df$values ~ df$internet)

abline(fit)

Call:

lm(formula = df$values ~ df$internet)

Residuals:

Min 1Q Median 3Q Max

-24393 -12278 -4654 6025 78528

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -77947 17786 -4.383 0.000102 ***

df$internet 1396 228 6.122 5.33e-07 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 19050 on 35 degrees of freedom

Multiple R-squared: 0.5171, Adjusted R-squared: 0.5033

F-statistic: 37.48 on 1 and 35 DF, p-value: 5.327e-07

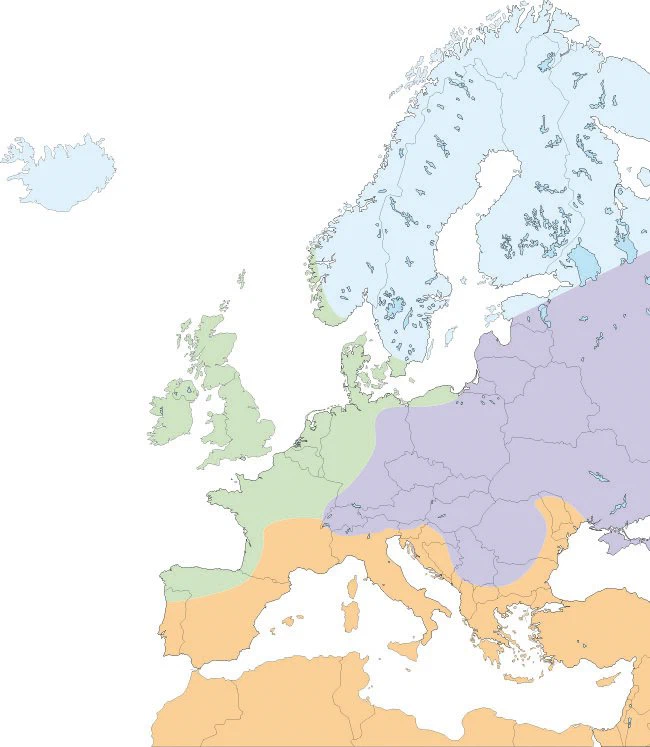

climate area

source: https://www.barenbrug.biz/forage/european-climate-zones

there are four climate zones on the map:

- Nordic climate (cold winters and mild humid summers)

- Eastern-continental climate (cold winters and hot summers)

- Oceanic climate (mild winters and humid summers)

- Mediterranean climate

for simplicity, merge 2 and 3 into one zone.

regressor analysis

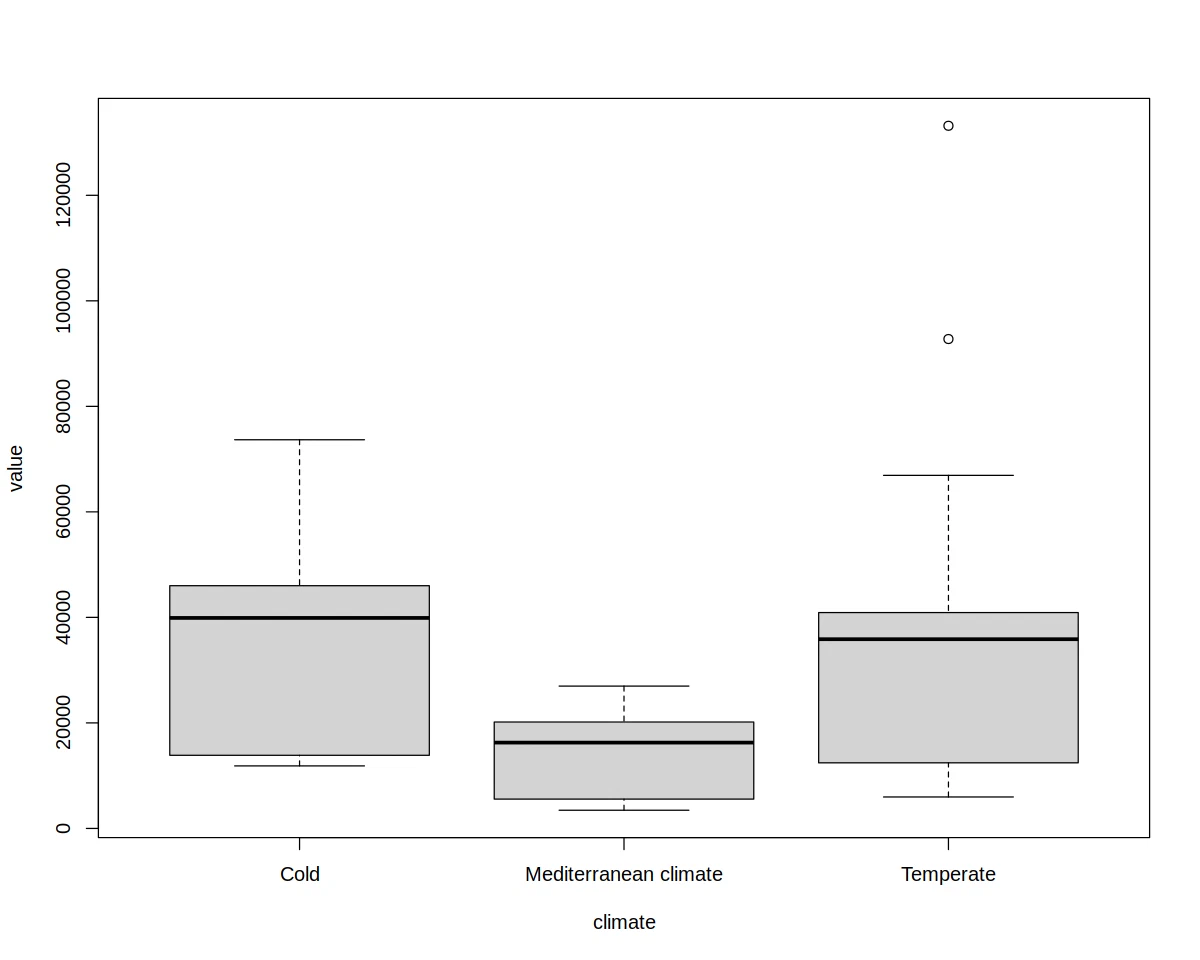

tapply(df$values, df$climate, summary)

$Cold

Min. 1st Qu. Median Mean 3rd Qu. Max.

11850 14550 39900 35632 45470 73670

$`Mediterranean climate`

Min. 1st Qu. Median Mean 3rd Qu. Max.

3450 5560 16270 13776 20170 26980

$Temperate

Min. 1st Qu. Median Mean 3rd Qu. Max.

5960 13260 35865 38620 40368 133180

options(repr.plot.width = 10, repr.plot.height = 6)

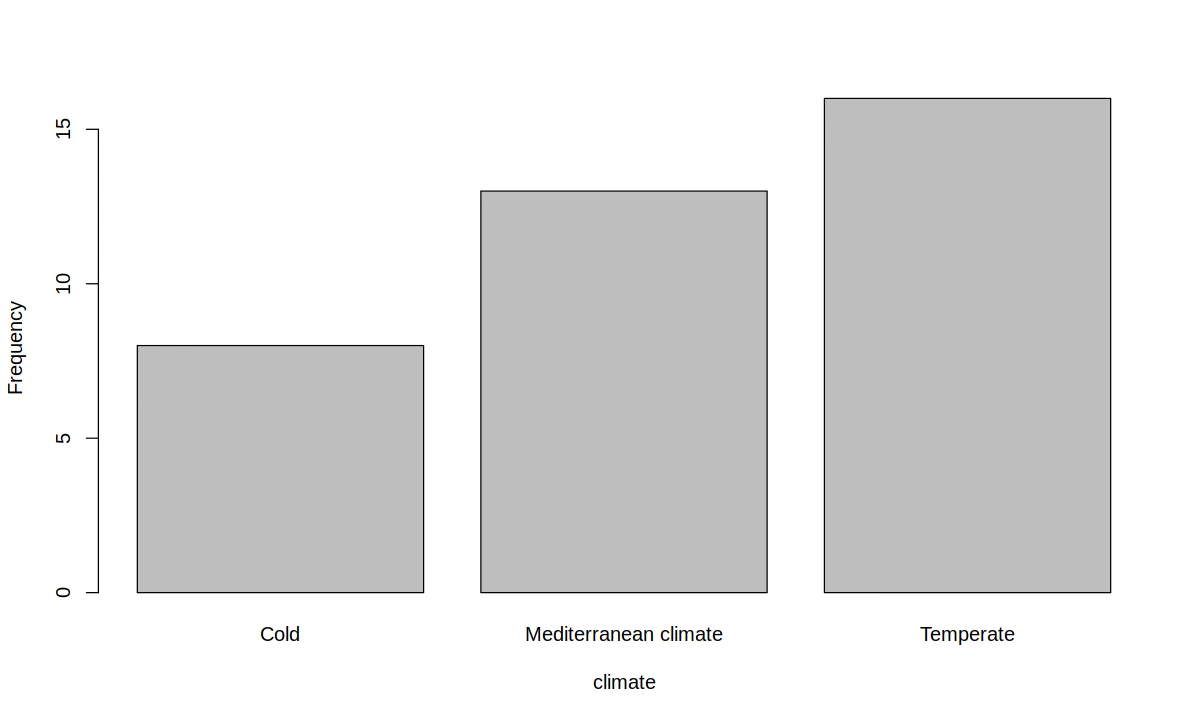

barplot(table(df$climate), xlab = "climate", ylab = "Frequency")

dependence on GDP

fit <- lm(df$values ~ df$climate)

summary(fit)

options(repr.plot.width = 10, repr.plot.height = 8)

boxplot(df$values ~ df$climate, ylab = "value", xlab = "climate")

Call:

lm(formula = df$values ~ df$climate)

Residuals:

Min 1Q Median 3Q Max

-32660 -10326 -2470 6394 94560

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 35632 8883 4.011 0.000314 ***

df$climateMediterranean climate -21856 11290 -1.936 0.061240 .

df$climateTemperate 2988 10880 0.275 0.785291

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 25130 on 34 degrees of freedom

Multiple R-squared: 0.1841, Adjusted R-squared: 0.1361

F-statistic: 3.836 on 2 and 34 DF, p-value: 0.03146

test whether the mean GDP is the same across climate regions or varies significantly.

\(H_0 : \mu_\text{cold} = \mu_\text{temperate} = \mu_\text{meditteranean}\)

\(H_A : H_0 \text{ does not hold.}\)

aov(df$values ~ df$climate)

anova(aov(df$values ~ df$climate))

Call:

aov(formula = df$values ~ df$climate)

Terms:

df$climate Residuals

Sum of Squares 4843358867 21464355258

Deg. of Freedom 2 34

Residual standard error: 25125.77

Estimated effects may be unbalanced

| Df | Sum Sq | Mean Sq | F value | Pr(>F) | |

|---|---|---|---|---|---|

| <int> | <dbl> | <dbl> | <dbl> | <dbl> | |

| df$climate | 2 | 4843358867 | 2421679433 | 3.835992 | 0.0314623 |

| Residuals | 34 | 21464355258 | 631304566 | NA | NA |

at the 5% level we reject the null hypothesis, mean GDP varies by climate region.

dependencies between regressors

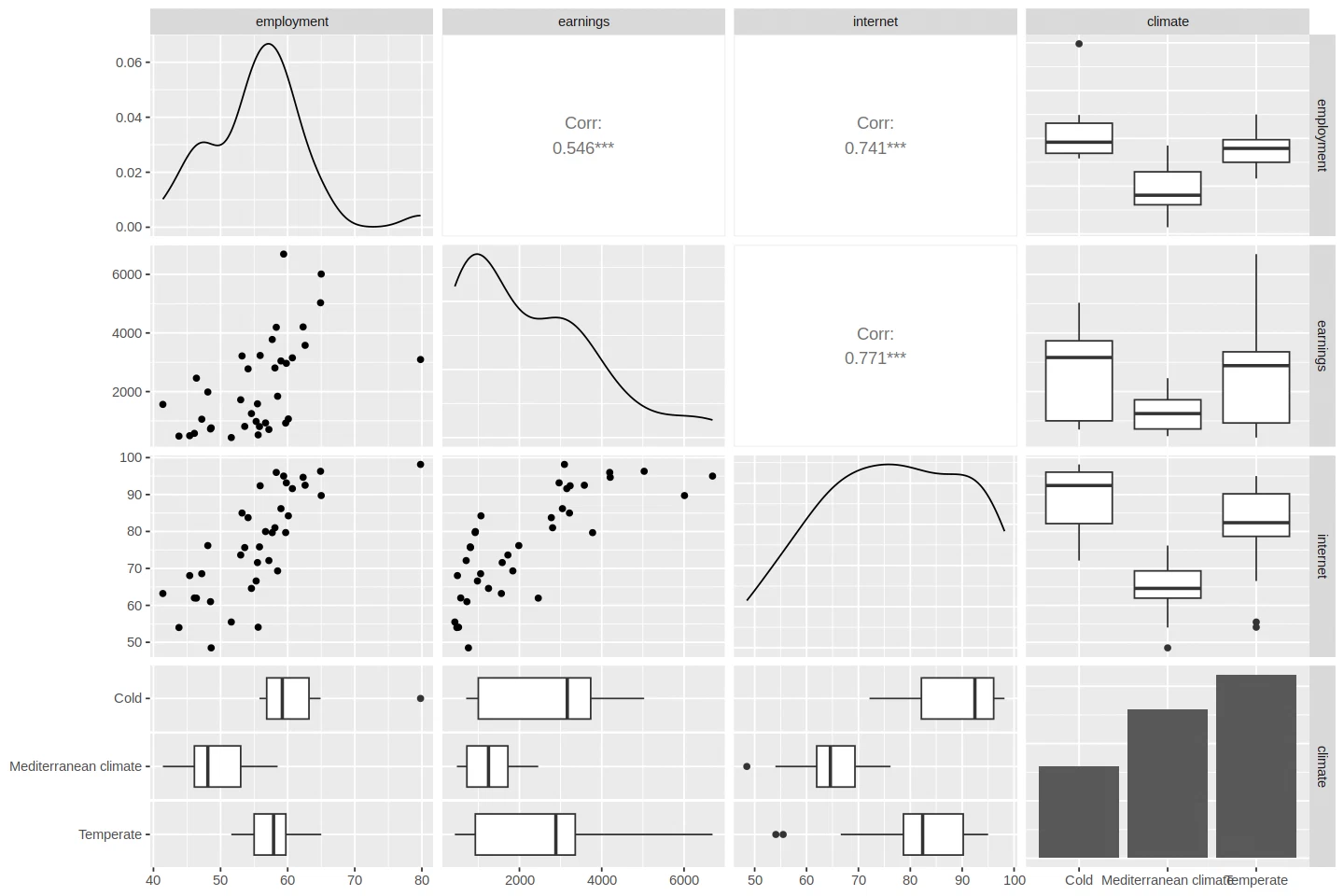

d <- subset(df, select = c("employment", "earnings", "internet", "climate"))

cor(d[c(1, 2, 3)])

options(repr.plot.width = 12, repr.plot.height = 8)

ggpairs(d, lower = list(combo = "box"))

| employment | earnings | internet | |

|---|---|---|---|

| employment | 1.0000000 | 0.5464316 | 0.7414445 |

| earnings | 0.5464316 | 1.0000000 | 0.7712457 |

| internet | 0.7414445 | 0.7712457 | 1.0000000 |

the correlations between the numerical indicators are statistically significant. there’s also a significant dependence on the categorical indicator (climate zone).

aov(df$employment ~ df$climate)

anova(aov(df$employment ~ df$climate))

Call:

aov(formula = df$employment ~ df$climate)

Terms:

df$climate Residuals

Sum of Squares 939.3983 933.4817

Deg. of Freedom 2 34

Residual standard error: 5.239785

Estimated effects may be unbalanced

| Df | Sum Sq | Mean Sq | F value | Pr(>F) | |

|---|---|---|---|---|---|

| <int> | <dbl> | <dbl> | <dbl> | <dbl> | |

| df$climate | 2 | 939.3983 | 469.69913 | 17.10775 | 7.229859e-06 |

| Residuals | 34 | 933.4817 | 27.45535 | NA | NA |

aov(df$earnings ~ df$climate)

anova(aov(df$earnings ~ df$climate))

Call:

aov(formula = df$earnings ~ df$climate)

Terms:

df$climate Residuals

Sum of Squares 17438893 77763451

Deg. of Freedom 2 34

Residual standard error: 1512.336

Estimated effects may be unbalanced

| Df | Sum Sq | Mean Sq | F value | Pr(>F) | |

|---|---|---|---|---|---|

| <int> | <dbl> | <dbl> | <dbl> | <dbl> | |

| df$climate | 2 | 17438893 | 8719446 | 3.812346 | 0.03207555 |

| Residuals | 34 | 77763451 | 2287160 | NA | NA |

aov(df$internet ~ df$climate)

anova(aov(df$internet ~ df$climate))

Call:

aov(formula = df$internet ~ df$climate)

Terms:

df$climate Residuals

Sum of Squares 3195.714 3787.583

Deg. of Freedom 2 34

Residual standard error: 10.5546

Estimated effects may be unbalanced

| Df | Sum Sq | Mean Sq | F value | Pr(>F) | |

|---|---|---|---|---|---|

| <int> | <dbl> | <dbl> | <dbl> | <dbl> | |

| df$climate | 2 | 3195.714 | 1597.8569 | 14.34348 | 3.041784e-05 |

| Residuals | 34 | 3787.583 | 111.3995 | NA | NA |

statistical modeling

with linear regression (or a variant of it), we’ll model GDP against all the chosen regressors, interpret the coefficients, and check the model’s quality. we’ll spot outliers, look at multicollinearity, and test the model assumptions. if the assumptions fail we’ll try something that compensates or drops them. the goal is a final sub-model that explains GDP well without insignificant pieces.

dependence of GDP on all regressors

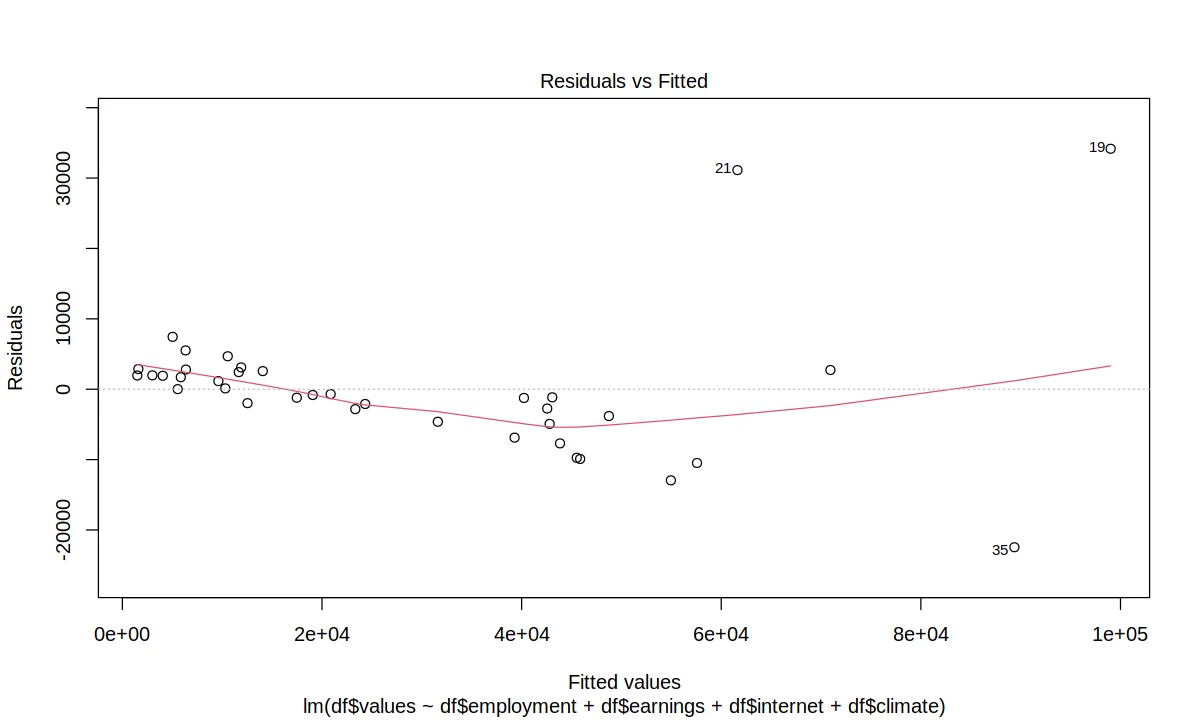

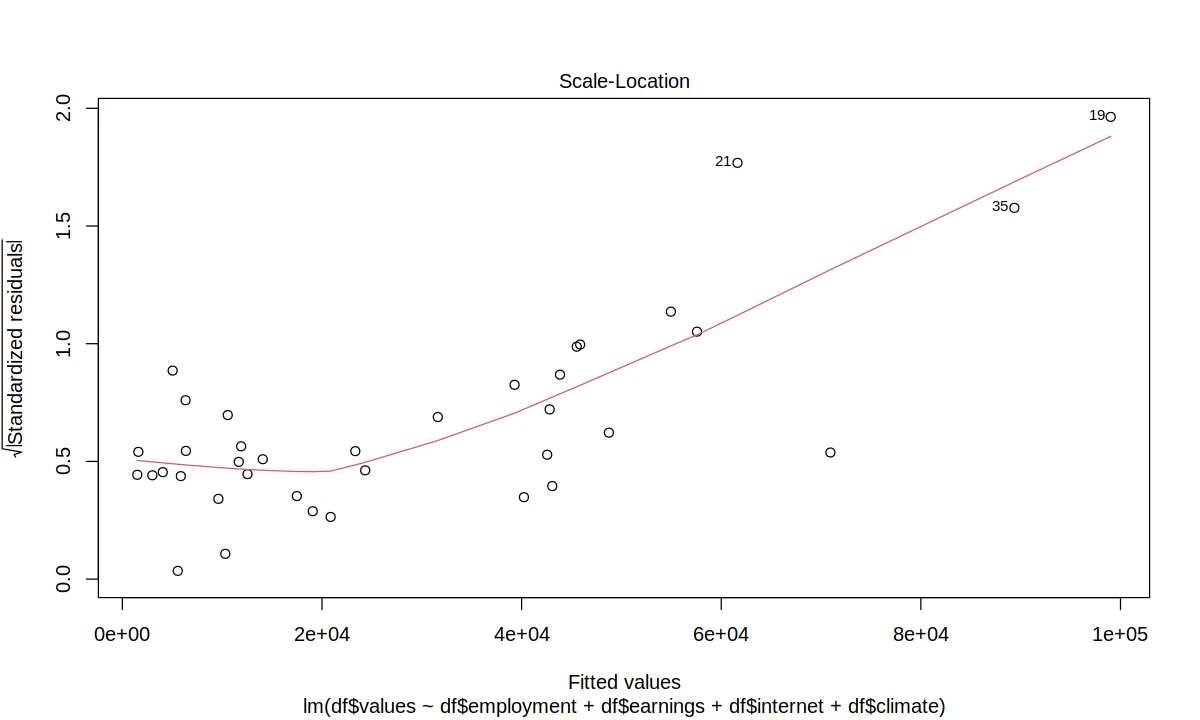

fit <- lm(df$values ~ df$employment + df$earnings + df$internet + df$climate)

summary(fit)

options(repr.plot.width = 10, repr.plot.height = 6)

plot(fit, which = 1)

plot(fit, which = 3)

Call:

lm(formula = df$values ~ df$employment + df$earnings + df$internet +

df$climate)

Residuals:

Min 1Q Median 3Q Max

-22452 -3813 -697 2572 34164

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -10160.722 25819.538 -0.394 0.697

df$employment 103.315 401.955 0.257 0.799

df$earnings 15.163 1.803 8.409 1.69e-09 ***

df$internet -19.648 273.609 -0.072 0.943

df$climateMediterranean climate 917.870 7153.894 0.128 0.899

df$climateTemperate 3433.730 5092.107 0.674 0.505

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 10590 on 31 degrees of freedom

Multiple R-squared: 0.8679, Adjusted R-squared: 0.8466

F-statistic: 40.72 on 5 and 31 DF, p-value: 1.004e-12

everything but “earnings” is statistically insignificant at the 5% level, so they can probably be dropped individually. the model could be refined by dropping regressors gradually, clustering them more broadly, or stepping back to simpler ones.

interpretation of the coefficients

- for every 1% increase in the employment rate, GDP goes up by €103.

- for every €1 increase in average monthly income, GDP goes up by €15.

- for every 1% increase in internet usage, GDP goes down by €20.

- in Nordic countries, with all regressors at zero, GDP at market prices is estimated at €-10,160 per capita. relative to that baseline, GDP is €917 higher in Mediterranean countries and €3,433 higher in temperate climate countries.

the current model isn’t great for the reasons above. there’s a multicollinearity problem, the regressors are highly correlated with each other, which distorts the individual coefficients and their significance. the model also has oddities like the negative relationship between internet usage and GDP, which doesn’t match intuition. and it’s sensitive to outliers, especially at high GDP, which we look at next.

outliers

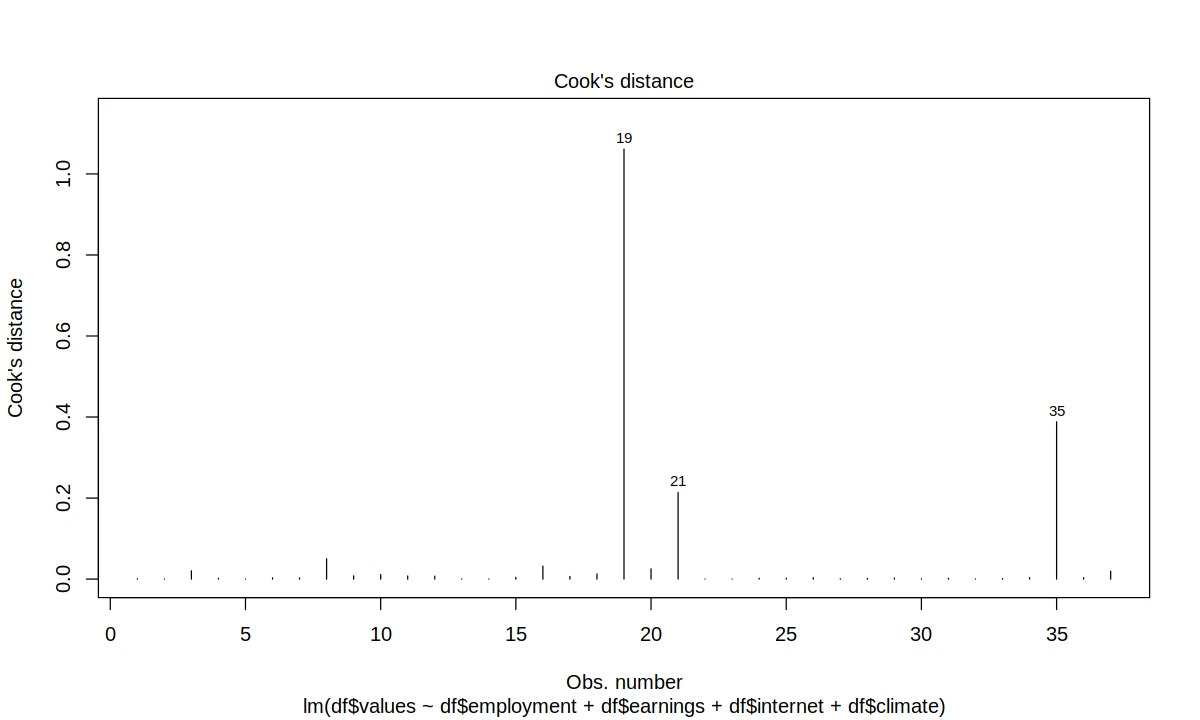

plot(fit, which = 4)

df[c(19, 21, 35), ]

| geo | values | employment | earnings | internet | climate | |

|---|---|---|---|---|---|---|

| <chr> | <dbl> | <dbl> | <dbl> | <dbl> | <fct> | |

| 19 | Liechtenstein | 133180 | 59.4 | 6692 | 95.00 | Temperate |

| 21 | Luxembourg | 92760 | 62.3 | 4206 | 94.67 | Temperate |

| 35 | Switzerland | 66920 | 65.0 | 6011 | 89.73 | Temperate |

the outliers are Liechtenstein, Luxembourg and Switzerland. relatively small countries with very strong financial sectors.

multicollinearity

conditionality of the matrix \(X^TX\)

Xnum <- df[, c("employment", "earnings", "internet")]

X <- as.matrix(Xnum)

XTX <- t(X) %*% X

XTX

cat("Singular values : ", round(svd(XTX)$d), "\n")

cat("Condition number: ", round(kappa(XTX, norm="2")))

| employment | earnings | internet | |

|---|---|---|---|

| employment | 115842.1 | 4750378 | 160384.7 |

| earnings | 4750378.1 | 274436377 | 6882837.6 |

| internet | 160384.7 | 6882838 | 225202.8 |

Singular values : 274691304 85341 777

Condition number: 497733

the matrix \(X^TX\) is very ill-conditioned (497733 \(\gg\) 1).

correlation

round(cor(Xnum), 3)

| employment | earnings | internet | |

|---|---|---|---|

| employment | 1.000 | 0.546 | 0.741 |

| earnings | 0.546 | 1.000 | 0.771 |

| internet | 0.741 | 0.771 | 1.000 |

the regressors are strongly correlated.

variance inflation factor

data.frame(round(vif(lm(df$values ~ df$employment + df$earnings + df$internet)), 3))

| round.vif.lm.df.values...df.employment...df.earnings...df.internet.... | |

|---|---|

| <dbl> | |

| df$employment | 2.229 |

| df$earnings | 2.477 |

| df$internet | 3.858 |

VIF isn’t too large for any of the regressors.

ridge regression

to dig further into multicollinearity, apply ridge regression and compare it with standard regression without regularization.

fit_rr <- lm.ridge(df$values ~ df$employment + df$earnings + df$internet + df$climate, lambda = 10)

fit_lm <- lm(df$values ~ df$employment + df$earnings + df$internet + df$climate)

data.frame(fit_lm$coef, coef(fit_rr, scale = FALSE))

| fit_lm.coef | coef.fit_rr..scale...FALSE. | |

|---|---|---|

| <dbl> | <dbl> | |

| (Intercept) | -10160.72250 | -30059.60907 |

| df$employment | 103.31457 | 189.79038 |

| df$earnings | 15.16323 | 9.93583 |

| df$internet | -19.64774 | 322.65346 |

| df$climateMediterranean climate | 917.87002 | 868.71395 |

| df$climateTemperate | 3433.72978 | 4206.47306 |

interpretation improves. internet usage gets a positive coefficient in the ridge regression model.

model assumptions

before using the diagnostic methods for submodel selection, a few assumptions need to hold.

regression model needs independent and equally distributed errors on top of a linear relationship between the explained and explanatory variables.

analysis of variance, like LR, needs independence and homogeneity of variances, and for the model selection method also normality of errors.

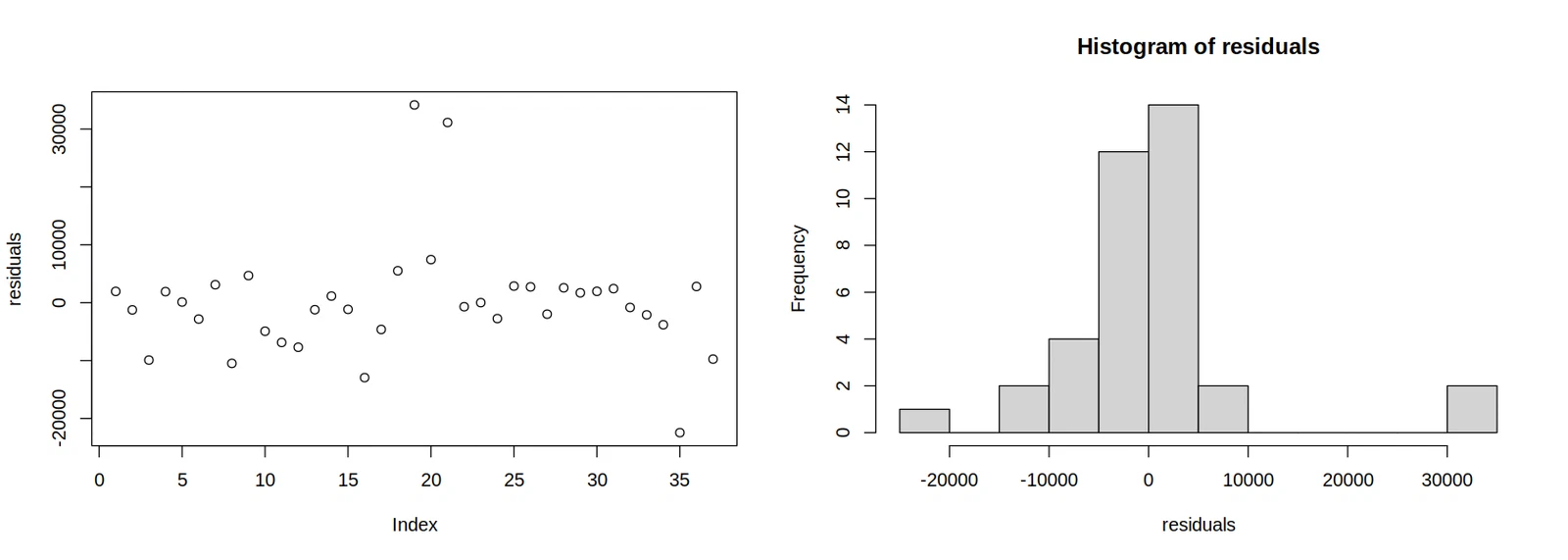

fit <- lm(df$values ~ df$employment + df$earnings + df$internet + df$climate)

residuals <- resid(fit)

options(repr.plot.width = 14, repr.plot.height = 5)

par(mfrow = c(1, 2))

plot(residuals)

hist(residuals, 10)

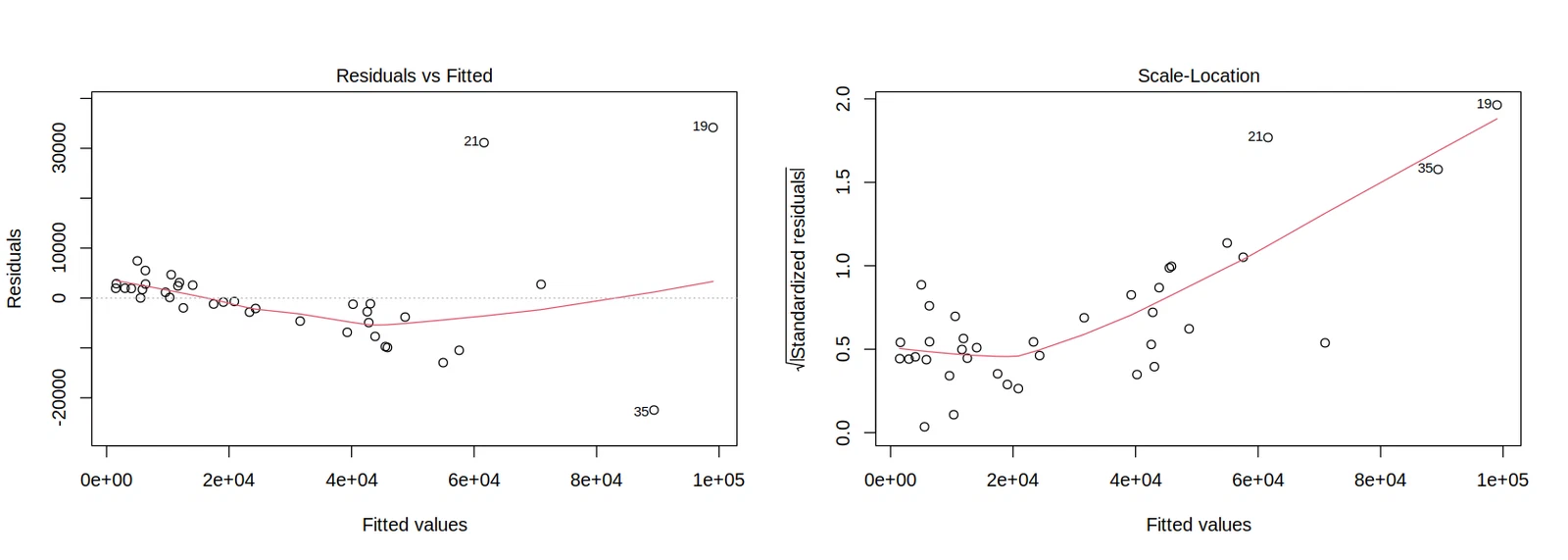

plot(fit, which = 1)

# plot(fit, which = 2)

plot(fit, which = 3)

# plot(fit, which = 4)

residue normality

the residual plot shows the residuals are distributed fairly symmetrically around zero.

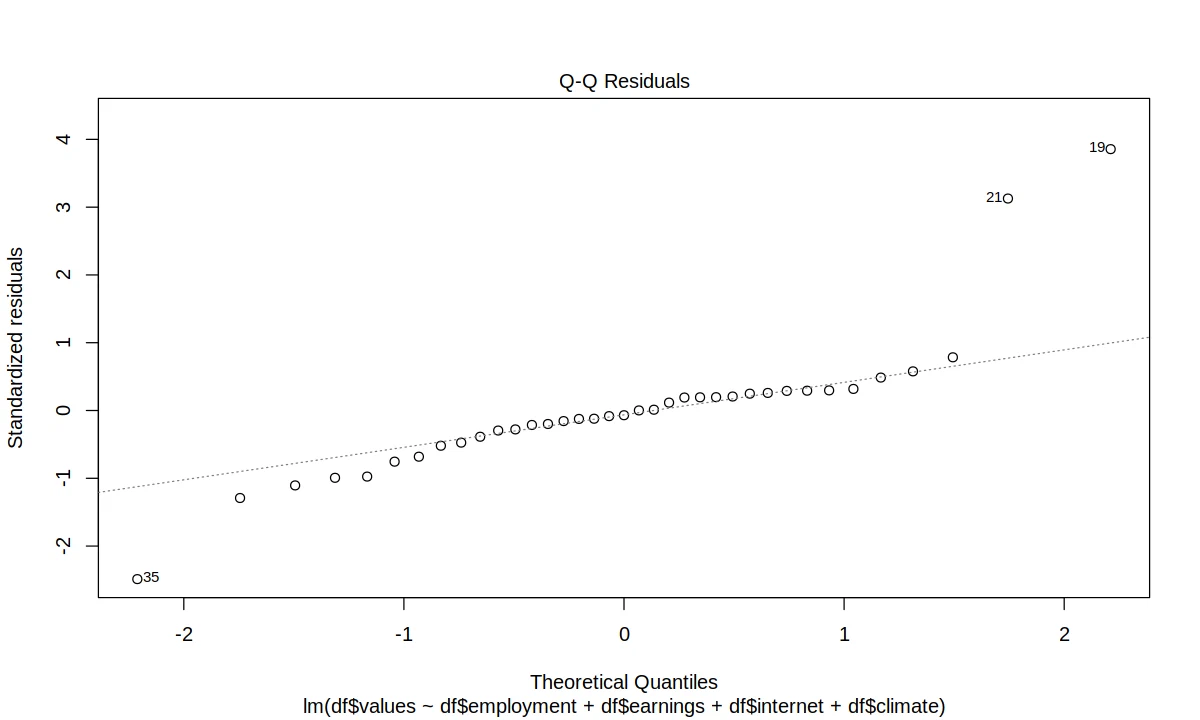

test the normality of the residuals with a Q-Q plot and the Shapiro-Wilk test.

\(H_0:\) The residuals come from a normal distribution.

\(H_A:\) The residuals do not come from a normal distribution.

shapiro.test(residuals)

options(repr.plot.width = 10, repr.plot.height = 6)

plot(fit, which = 2)

Shapiro-Wilk normality test

data: residuals

W = 0.79839, p-value = 1.21e-05

at the 5% level we reject the normality of the residuals.

homogeneity of variance of residuals

test the homogeneity of the residual variance with the Breusch-Pagan test.

\(H_0:\) The residuals have identical variances.

\(H_A:\) The residuals do not have identical variances.

bptest(fit)

studentized Breusch-Pagan test

data: fit

BP = 18.577, df = 5, p-value = 0.002303

at the 5% level, the homogeneity of variances of the initial model is rejected.

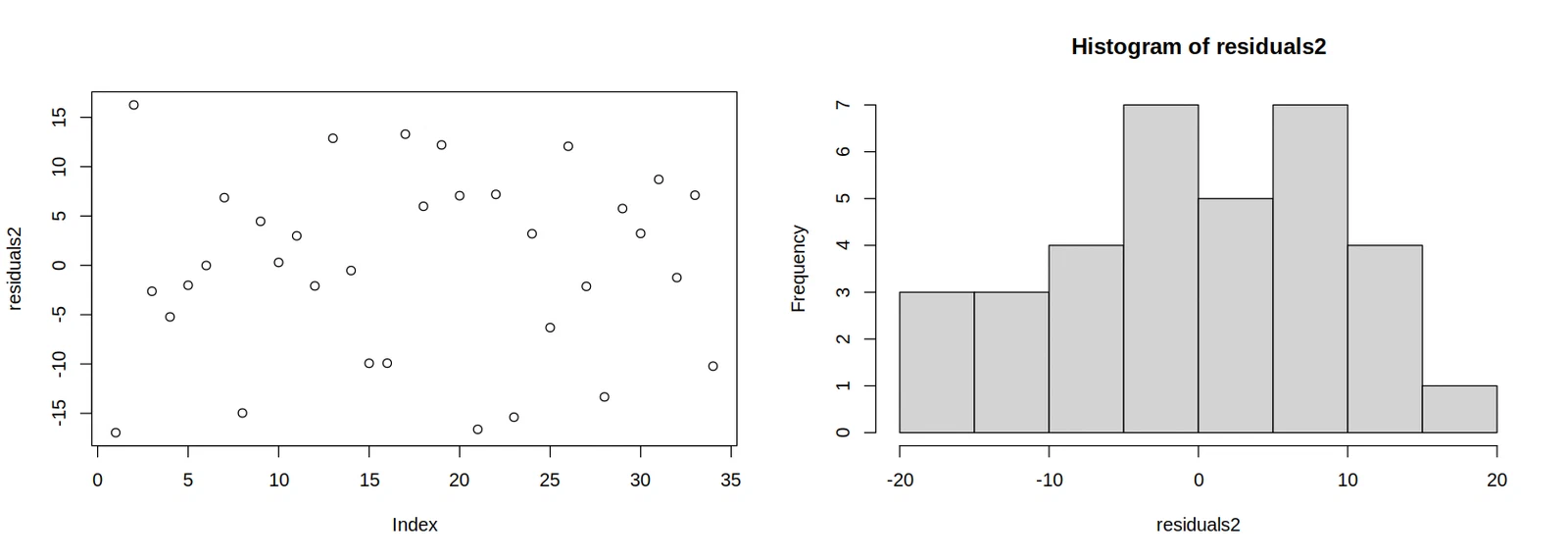

correction

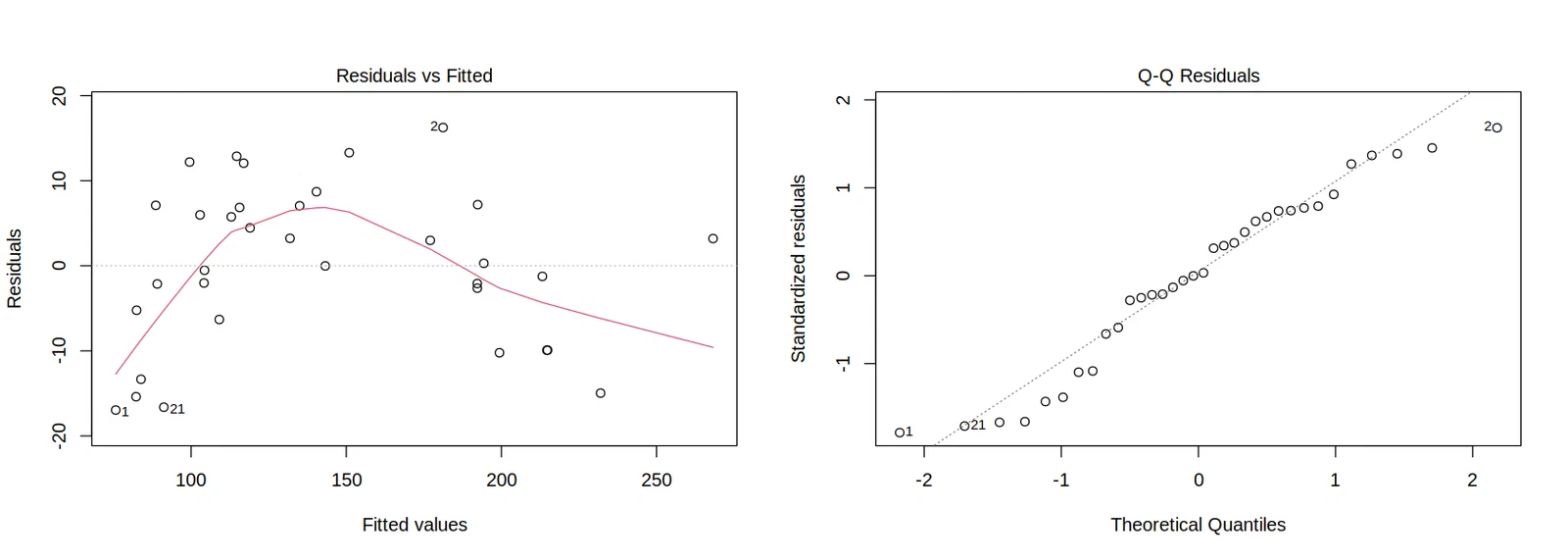

since the residuals grow with the explanatory variable, transform the GDP values. we take the square root and drop the outliers that stand out from the rest.

df2 <- df[-c(19, 21, 35),]

df2$values <- sqrt(df2$values)

fit2 <- lm(df2$values ~ df2$employment + df2$earnings + df2$internet + df2$climate)

summary(fit2)

residuals2 <- resid(fit2)

options(repr.plot.width = 14, repr.plot.height = 5)

par(mfrow = c(1, 2))

plot(residuals2)

hist(residuals2, 10)

plot(fit2, which = 1)

plot(fit2, which = 2)

Call:

lm(formula = df2$values ~ df2$employment + df2$earnings + df2$internet +

df2$climate)

Residuals:

Min 1Q Median 3Q Max

-16.9576 -6.0405 0.1392 7.0079 16.2545

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -4.54867 25.28852 -0.180 0.8585

df2$employment 0.97844 0.39462 2.479 0.0194 *

df2$earnings 0.03548 0.00229 15.494 2.89e-15 ***

df2$internet 0.31952 0.28165 1.134 0.2662

df2$climateMediterranean climate 3.10285 6.96468 0.446 0.6594

df2$climateTemperate 3.46487 5.08587 0.681 0.5013

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 10.15 on 28 degrees of freedom

Multiple R-squared: 0.969, Adjusted R-squared: 0.9634

F-statistic: 174.8 on 5 and 28 DF, p-value: < 2.2e-16

residue normality

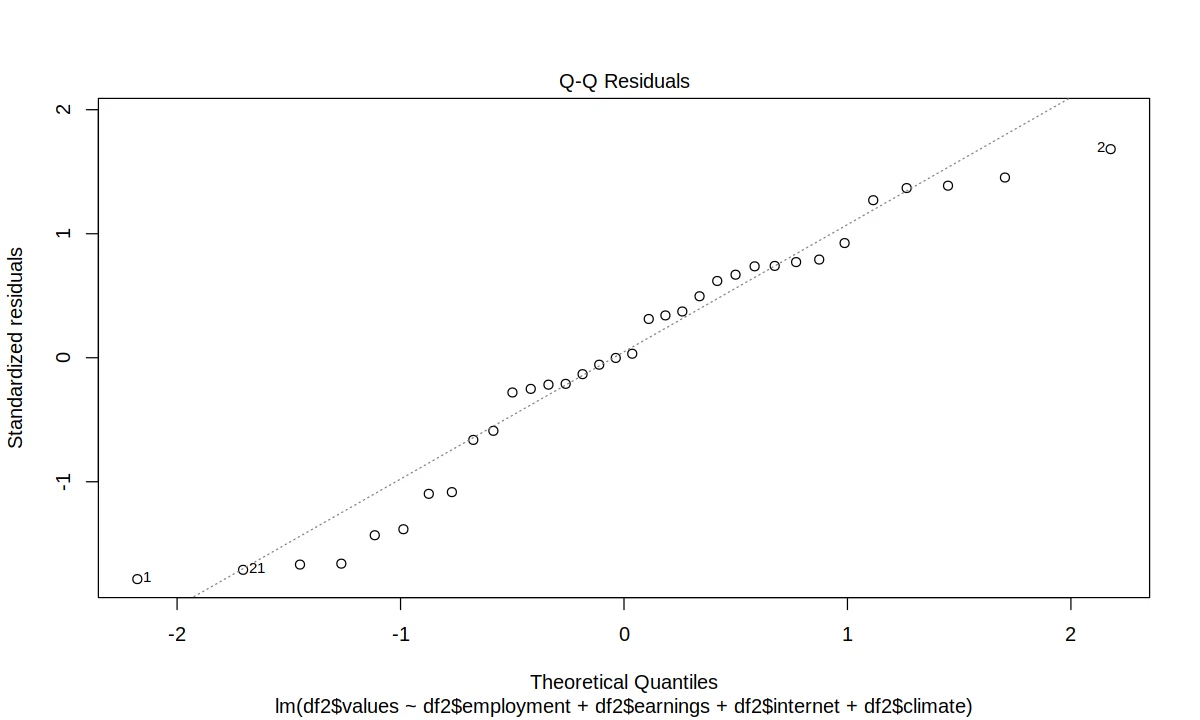

shapiro.test(residuals2)

options(repr.plot.width = 10, repr.plot.height = 6)

plot(fit2, which = 2)

Shapiro-Wilk normality test

data: residuals2

W = 0.95774, p-value = 0.2088

here, at the 5% level, we fail to reject the normality of residuals.

homogeneity of variance of residuals

bptest(fit2)

studentized Breusch-Pagan test

data: fit2

BP = 6.0235, df = 5, p-value = 0.3039

here too, at the 5% level, we fail to reject the homogeneity of residual variance.

choosing the final model

picking the final model now. it should be accurate, but we’d rather have one that’s simple and easy to interpret.

start with a model that has all the regressors, then simplify as we go. the final model should explain the variable well and have no insignificant pieces.

we’ll work with an all-flags model, transformed response, no outliers.

fit_overparam <- lm(df2$values ~ df2$employment + df2$earnings + df2$internet + df2$climate)

summary(fit_overparam)

Call:

lm(formula = df2$values ~ df2$employment + df2$earnings + df2$internet +

df2$climate)

Residuals:

Min 1Q Median 3Q Max

-16.9576 -6.0405 0.1392 7.0079 16.2545

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -4.54867 25.28852 -0.180 0.8585

df2$employment 0.97844 0.39462 2.479 0.0194 *

df2$earnings 0.03548 0.00229 15.494 2.89e-15 ***

df2$internet 0.31952 0.28165 1.134 0.2662

df2$climateMediterranean climate 3.10285 6.96468 0.446 0.6594

df2$climateTemperate 3.46487 5.08587 0.681 0.5013

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 10.15 on 28 degrees of freedom

Multiple R-squared: 0.969, Adjusted R-squared: 0.9634

F-statistic: 174.8 on 5 and 28 DF, p-value: < 2.2e-16

the R-squared of 0.96 is very good, but a lot of the coefficients are insignificant, so we should try to simplify.

test model-submodel

test whether a richer model can be reduced to a simpler submodel. use a sequential procedure with the smallest and largest sets of parameters below.

- smallest:

HDP' ~ 1(constant) - largest:

HDP' ~ employment + earnings + internet + climate

step(lm(df2$values ~ 1), trace=T, scope = list(

lower = ~1,

upper = ~df2$values ~ df2$employment + df2$earnings + df2$internet + df2$climate

))

Start: AIC=271.08

df2$values ~ 1

Df Sum of Sq RSS AIC

+ df2$earnings 1 88288 4714 171.69

+ df2$internet 1 64228 28774 233.19

+ df2$employment 1 35915 57087 256.48

+ df2$climate 2 24387 68615 264.74

<none> 93002 271.08

Step: AIC=171.69

df2$values ~ df2$earnings

Df Sum of Sq RSS AIC

+ df2$employment 1 1661 3053 158.92

+ df2$internet 1 1089 3625 164.75

+ df2$climate 2 730 3984 169.97

<none> 4714 171.69

- df2$earnings 1 88288 93002 271.08

Step: AIC=158.92

df2$values ~ df2$earnings + df2$employment

Df Sum of Sq RSS AIC

<none> 3053 158.92

+ df2$internet 1 118 2935 159.58

+ df2$climate 2 33 3020 162.55

- df2$employment 1 1661 4714 171.69

- df2$earnings 1 54034 57087 256.48

Call:

lm(formula = df2$values ~ df2$earnings + df2$employment)

Coefficients:

(Intercept) df2$earnings df2$employment

8.96734 0.03727 1.15468

fit_reduced_1 <- lm(df2$values ~ df2$earnings + df2$employment)

summary(fit_reduced_1)

Call:

lm(formula = df2$values ~ df2$earnings + df2$employment)

Residuals:

Min 1Q Median 3Q Max

-18.6950 -7.1481 0.3365 9.1403 16.8266

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 8.967342 14.205352 0.631 0.532495

df2$earnings 0.037269 0.001591 23.423 < 2e-16 ***

df2$employment 1.154683 0.281167 4.107 0.000271 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 9.924 on 31 degrees of freedom

Multiple R-squared: 0.9672, Adjusted R-squared: 0.9651

F-statistic: 456.7 on 2 and 31 DF, p-value: < 2.2e-16

the sequential selection stopped at the lowest-AIC model, GDP' ~ earnings + employment, but the intercept is still insignificant at the 5% level.

# -intercept

fit_reduced_2 <- lm(df2$values ~ 0 + df2$earnings + df2$employment)

summary(fit_reduced_2)

Call:

lm(formula = df2$values ~ 0 + df2$earnings + df2$employment)

Residuals:

Min 1Q Median 3Q Max

-17.1454 -7.1348 0.7599 8.8256 16.7243

Coefficients:

Estimate Std. Error t value Pr(>|t|)

df2$earnings 0.036914 0.001474 25.04 <2e-16 ***

df2$employment 1.327927 0.060566 21.93 <2e-16 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 9.83 on 32 degrees of freedom

Multiple R-squared: 0.9961, Adjusted R-squared: 0.9958

F-statistic: 4068 on 2 and 32 DF, p-value: < 2.2e-16

this simplification got rid of all the irrelevant components.

quality comparison, the R-squared values during this gradual simplification are interesting.

| Fit | Model | R-squared | Adjusted R-squared |

|---|---|---|---|

| fit_overparam | HDP’ ~ … | 0.969 | 0.963 |

| fit_reduced_1 | HDP’ ~ earnings + employment | 0.967 | 0.965 |

| fit_reduced_2 | HDP’ ~ 0 + earnings + employment | 0.996 | 0.996 |

the last model has the highest adjusted R-squared.

test model-submodel

anova(fit_reduced_2,

fit_reduced_1,

fit_overparam,

test="F")

| Res.Df | RSS | Df | Sum of Sq | F | Pr(>F) | |

|---|---|---|---|---|---|---|

| <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | <dbl> | |

| 1 | 32 | 3092.262 | NA | NA | NA | NA |

| 2 | 31 | 3053.017 | 1 | 39.24559 | 0.3805883 | 0.5422729 |

| 3 | 28 | 2887.311 | 3 | 165.70569 | 0.5356494 | 0.6616838 |

more complex models can be reduced to the submodel GDP' ~ 0 + earnings + employment without a significant accuracy loss.

final model

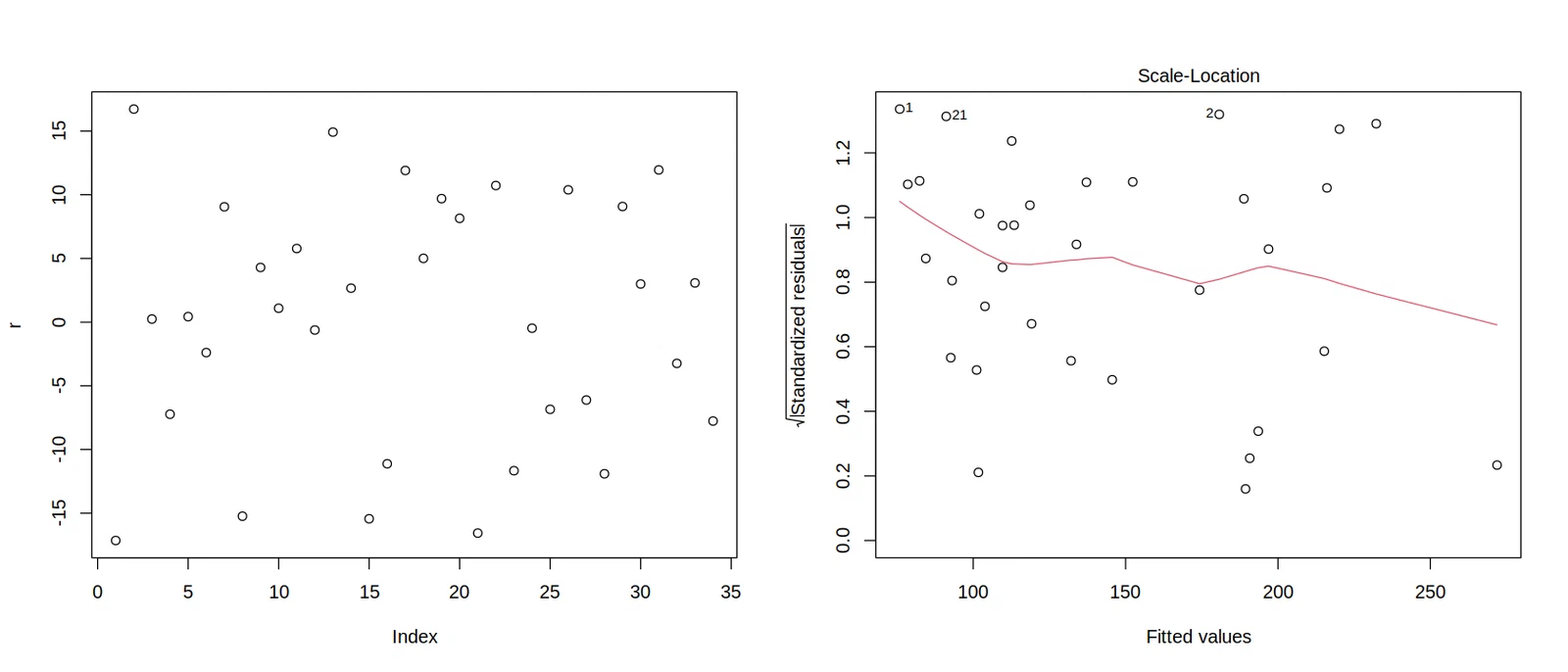

m <- lm(df2$values ~ 0 + df2$earnings + df2$employment)

r <- resid(m)

summary(m)

options(repr.plot.width = 14, repr.plot.height = 6)

par(mfrow = c(1, 2))

plot(r)

plot(m, which = 3)

Call:

lm(formula = df2$values ~ 0 + df2$earnings + df2$employment)

Residuals:

Min 1Q Median 3Q Max

-17.1454 -7.1348 0.7599 8.8256 16.7243

Coefficients:

Estimate Std. Error t value Pr(>|t|)

df2$earnings 0.036914 0.001474 25.04 <2e-16 ***

df2$employment 1.327927 0.060566 21.93 <2e-16 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 9.83 on 32 degrees of freedom

Multiple R-squared: 0.9961, Adjusted R-squared: 0.9958

F-statistic: 4068 on 2 and 32 DF, p-value: < 2.2e-16

with zero income and zero employment, GDP is zero. for every percent of employment, the square root of GDP increases by 1.33, and for every euro in average income, GDP increases by 0.04.

the final model is fine. it has a high R-squared, doesn’t make systematic errors, and is fairly simple. unlike the earlier models, it also gives valid values at low regressor levels.